TL;DR

- A password manager stores login credentials. It does not tell your family what accounts exist, what each one is for, or what to do when a verification code goes to a phone they cannot unlock.

- Most households have covered two of the three things family continuity requires: legal documents and stored credentials. What is almost always missing is the operational layer, which is a current and organized record of what exists and what your family should actually do with it.

- Financial accounts accumulate faster than anyone documents them. Families regularly discover accounts nobody knew about, sometimes months after a loss. Over $77 billion in unclaimed assets sits in US state treasuries for exactly this reason.

- When an employee loses a family member, the impact does not end at bereavement leave. Many grieving employees spend four or more hours per week on financial and legal tasks during work hours for weeks or months after the loss. Grief-related productivity loss costs US employers an estimated $75 billion every year.

- Incapacity is statistically more common during working years than death. It creates the same information crisis for a family, with none of the legal clarity a death certificate provides.

- SmartHeritance builds the operational layer for individuals and offers it as a low-cost, high-impact employee benefit. It provides automatic account discovery, a secure continuity record, and a verified delivery process that ensures information reaches the right people when they need it.

Introduction

Most people who use a password manager feel reasonably organized because their credentials are stored securely, a master password may be shared with a spouse, and important legal documents are somewhere on file. From the outside, it feels as though the family has a general understanding of where everything is and how it can be accessed.

For HR and benefits leaders, the picture looks similarly complete on paper. Life insurance is in place, an EAP is available, and bereavement leave policies are documented. The employee benefits stack appears to cover the major financial and emotional bases.

Both situations appear complete on the surface, but the gaps only become visible during a crisis, especially when someone is trying to manage a family loss while also handling professional responsibilities.

This article is about the gap between having a password manager, or a benefits package, and having a system that actually works for a family in crisis. The missing piece is what can be described as the operational layer, and very few systems have been designed to address it properly.

What Password Managers Actually Do

Password managers were built to stop people who should not have access from getting in. They solve problems like credential theft, phishing attacks, and the risks of reusing passwords across dozens of platforms. According to NordPass’s 2024 research, the average person manages around 168 personal passwords, and without a dedicated tool, keeping those secure is nearly impossible.

Password managers solve that problem well because they were designed to protect accounts from unauthorized access. They help people manage hundreds of passwords securely while reducing the risks of phishing, credential theft, and password reuse across platforms.

But your family is not an unauthorized actor. They are the people who may need legitimate access to a financial life they were never fully shown, at a moment when you may no longer be able to guide them through it.

That creates a fundamentally different problem. Securing access is one challenge. Helping a family understand what exists, where to find it, and what to do next during a crisis is another entirely.

Common Access Problems Families Face During Emergencies

Two-Factor Authentication Locks Your Family Out

Most financial accounts now send a verification code to your phone when someone logs in from a new device. If you are hospitalized and your phone is locked in a hospital room, your spouse may have the password but still cannot complete the login.

The security system is doing exactly what it was designed to do, which is why families often struggle to work around it during emergencies. The protections are functioning correctly, but they were never designed for situations where legitimate family members suddenly need urgent access.

Some accounts require a court order to resolve this. Others require a death certificate and weeks of processing. People who have been through it describe it the same way: they had the password, but the code went somewhere they could not reach.

Incomplete Financial Records Create Problems for Families

A password manager only contains what you deliberately added to it. In reality, very few people consistently add every account they open or every service they sign up for.

That includes retirement accounts from previous employers, brokerage accounts that went dormant, life insurance policies purchased years ago, or subscriptions that have been quietly renewing from cards nobody actively monitors.

None of these appear in a password manager unless you consciously added them.

According to a 2026 survey by DK Law Group, Americans value their personal digital assets at more than $190,000 on average. More than $77 billion sits in US state treasuries as unclaimed property. Families cannot claim what they cannot find, and a password manager cannot show them what was never added to it.

Access Without Context Is Not Enough

Even when a family gets into an account, they often do not know what they are looking at or what to do next.

Which bank account does the mortgage pull from automatically? Which investment accounts carry tax consequences if withdrawn early? Which recurring monthly charges should continue? Who is the financial advisor and how do you reach them?

A credential may help your family access an account, but access alone does not provide the context they need to understand what they are looking at or what actions they should take next.

Outdated Records Create Invisible Gaps

A password manager reflects the last time you updated it.

New accounts get opened. Insurance providers change. Beneficiary designations go unreviewed after major life events. Subscriptions move platforms.

Each change creates a gap between what the record says and what is actually true. During normal life, no one notices because you are still managing everything. The record only gets tested when you are no longer available to fill in what is missing.

Incapacity Is the Scenario Nobody Plans For

A stroke, a serious accident, or a cognitive condition that progresses quickly can create the same information problem for your family as death, with one major difference: there is no death certificate to trigger legal processes.

A family managing a sudden hospitalization needs access to financial information immediately while also coordinating medical care and keeping their own lives running. The will has not been triggered. The estate process has not started. The knowledge you carry in your head about your financial life is not accessible to anyone else.

Despite how common these situations are, very few planning tools are designed to address them directly.

For employers, this scenario is equally overlooked. An employee managing a parent’s sudden incapacitation does not disappear from the workforce for a defined bereavement period. They continue showing up while spending hours each week on financial and administrative tasks that have no clear end date and no policy designed to support them.

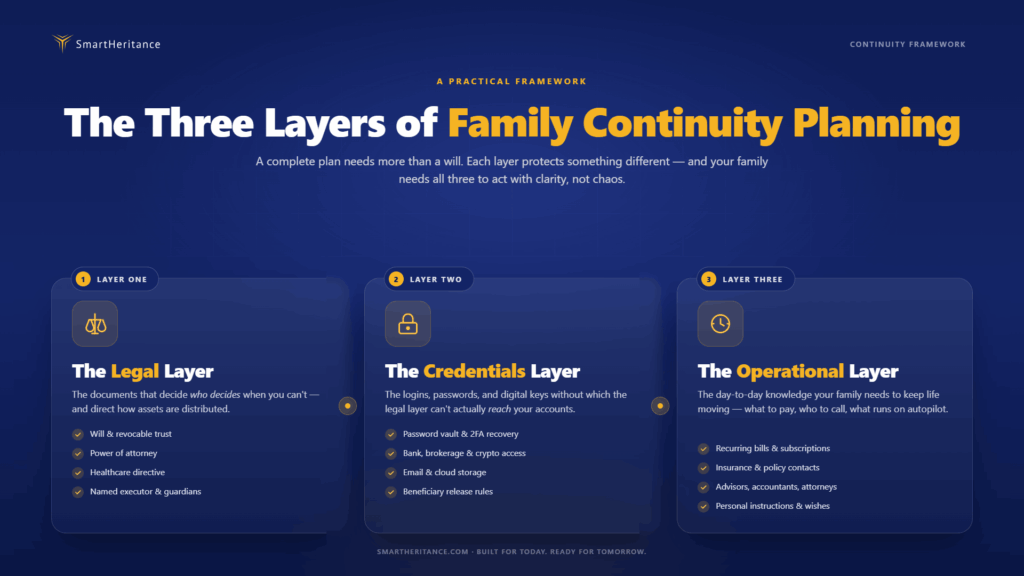

The Three Layers of Family Continuity Planning

Most organized households, and most benefits packages, have covered two of the three layers family continuity requires.

- The Legal Layer: The legal layer includes wills, trusts, and powers of attorney. It establishes who has authority and how assets should be distributed.

- The Credential Layer: The credential layer includes password managers and stored login information. Organized individuals usually address this layer with genuine effort.

- The Operational Layer: The operational layer is the system that tells a family what accounts exist, what each one is for, the order in which actions need to happen, and what information is current.

More importantly, it is the only layer that answers the first question most families ask during a crisis: where do we even start?

The legal layer tells families who gets what. The credential layer gives them a way in. The operational layer is what makes both usable under pressure.

Without it, a family with a thorough will and a thorough password manager still has to reconstruct a financial life they were never shown while managing everything else a crisis brings.

For employers, that reconstruction process directly impacts workforce productivity. Nearly half of employees report a decline in work performance after a family loss. Many spend four or more hours each week handling estate and financial tasks during work hours for weeks or months after returning from leave.

SmartHeritance fills the operational layer for both individuals building their own continuity record and employers offering it as a benefit that reduces personal burden and organizational disruption.

How SmartHeritance Builds the Operational Layer

SmartHeritance is a Family Continuity Platform.

Individuals use it to organize and maintain a complete record of their financial and digital life. Employers offer it as a benefit that gives employees something no standard benefits package currently provides: operational infrastructure their families can rely on when something goes wrong.

SmartSync: Automatic Account Discovery

When you connect SmartHeritance to your Gmail, Outlook, or Yahoo account, SmartSync scans your inbox for correspondence from financial institutions, insurance providers, retirement platforms, investment services, and subscription platforms.

It is looking specifically for the accounts that make up your financial life. Personal emails are never accessed or stored.

What SmartSync finds is surfaced for your review. You approve what gets added to your record, and nothing is stored without your approval.

Most people discover accounts during the first scan that they had genuinely stopped thinking about. These often include retirement funds from previous employers, insurance policies purchased years ago, or brokerage accounts that went dormant.

These are often the exact accounts families spend weeks trying to identify and track down after a loss, whereas SmartSync is designed to surface them within minutes during the setup process.

After the initial setup, SmartSync continues scanning every few months. When you open a new bank account, take out a new insurance policy, or sign up for a new service, the confirmation email lands in your inbox and SmartSync identifies it automatically.

As a result, the continuity record stays current without requiring people to manually remember and update every financial or digital change in their lives.

Your Secure Digital Vault

SmartHeritance provides a private and organized place to store everything your family would need.

This includes:

- Bank accounts and investment portfolios

- Insurance policies and retirement funds

- Property documents and vehicle records

- Login credentials and digital assets including cryptocurrency

- Legal documents like wills and powers of attorney

- Medical information and emergency contacts

- Final wishes, video messages, and personal instructions

Everything is organized by category and accessible only to you while you are alive. You decide what gets shared, who receives it, and when.

The platform is built on AES-256 encryption, which is the same standard used by banks and governments. Nobody at SmartHeritance, including support or engineering teams, can access what you store.

The architecture is intentionally designed so your data remains inaccessible even internally.

SmartHeritance is also Google CASA Tier 2 certified, meaning its security and compliance standards have been independently verified.

Designating Trusted Recipients

For each category of information you store, you choose who receives it and under what conditions.

A spouse may receive everything. An adult child may receive only information tied to specific accounts. A trusted friend may receive instructions intended to remain separate from family.

Information is not shared broadly or casually. Instead, it is assigned carefully to specific people, for clearly defined purposes, under conditions you control.

Wellness Check Protocol: Verified Information Delivery

Organizing your information is only one part of the problem. Ensuring it reaches your family at the right moment is the other part, and it is the part most tools ignore entirely.

The Wellness Check Protocol monitors your activity on the platform quietly in the background.

As long as you remain active, nothing happens. If there is an extended period of inactivity, the system sends you a direct check-in. If you respond, the clock resets.

If you do not respond, the system reaches out to the family members you designated.

If your family confirms something has happened and provides the required verification, your record is released to the people you selected under the exact conditions you defined.

Your family does not need to remember the platform exists or search for login details in the middle of a crisis. The system is designed to reach the right people, verify the situation appropriately, and deliver the information your family needs without forcing them to search for it themselves.

Parent Account

If you have aging parents whose financial records are not organized, SmartHeritance allows you to create and manage a continuity record on their behalf.

You handle the setup and maintenance, while the information still belongs to your parent and is released according to their designations.

It is a practical way for adult children to ensure the entire family is prepared, not just their own household.

What This Means for HR and Benefits Leaders

The case for offering SmartHeritance as an employee benefit is operational, not just compassionate.

When an employee’s family is disorganized at the moment of loss, the disruption extends far beyond bereavement leave. Employees return to work while still carrying the administrative burden of reconstructing a financial life.

In many cases, that burden continues for weeks or even months after the employee has officially returned to work.

It appears as distraction, reduced output, unplanned absences, and in some cases, turnover from employees who simply cannot manage both responsibilities at once.

SmartHeritance addresses this problem at the source.

When employees already have an organized continuity record in place before a crisis occurs, the administrative burden their families face is dramatically reduced. That translates directly into shorter and less disruptive post-loss recovery periods inside the workplace.

From a deployment standpoint, SmartHeritance is straightforward to implement. Employee accounts are pre-provisioned, onboarding happens through a custom enrollment URL, and HR teams receive enrollment and usage metrics without visibility into what employees actually store.

There is no ongoing administrative burden for the People team once the benefit is live.

At $7.50 to $8.99 per employee per month, it is one of the lowest-cost additions to a benefits stack relative to the problem it solves.

It sits alongside life insurance and financial wellness programs as the layer that makes those existing benefits usable when families need them most.

For benefits leaders looking to differentiate their package, SmartHeritance offers something most competitors are not yet offering: continuity, not just coverage.

Addressing Common Objections

“My spouse already knows where everything is”

- They know what you have told them.

- Families navigating a loss consistently discover accounts, policies, and subscriptions nobody knew existed.

- General awareness is not the same as having a current and organized record.

“I already have a will”

- A will establishes who receives assets.

- It does not tell your family where those assets are held, how to access them, or what to do during the first week after a crisis.

- A will and a continuity system solve two entirely different problems. One defines inheritance. The other helps families actually locate and access what exists.

“I already use a password manager”

- The credential layer is only one of three layers.

- It covers accounts you deliberately added.

- It cannot surface forgotten accounts, generate verification codes sent to a locked phone, or explain what decisions your family should make after gaining access.

“We already offer life insurance”

- Life insurance answers whether a family will be financially protected.

- SmartHeritance answers whether they will know what exists, where to find it, and what to do next.

- The two benefits address closely related problems and become significantly more effective when offered together.

“This is only for wealthy families”

- Account complexity scales with how long someone has been online, not how much money they have.

- The discoverability and access problem exists regardless of asset value.

“Incapacity planning feels premature”

- Strokes and serious accidents during working years are statistically more common than death during the same period.

- The scenario most people postpone planning for is often the more likely one.

- It is also the scenario that creates the longest sustained disruption in the workplace.

The Missing Layer in Your Family’s Plan

A will and a password manager are both necessary. A life insurance policy and an EAP are both necessary.

What none of them provide is the operational layer: the organized, current, and deliverable record of what a financial life actually looks like and what a family should do with it.

That is the layer SmartHeritance builds.

It finds what exists, keeps the record current, stores everything a family would need in one secure place, and delivers it to the right people at the right time through a verified process.

For individuals, it means families are given a clear starting point instead of being forced to reconstruct an entire financial life during an already overwhelming period.

For employers, it creates a benefit that reduces operational disruption, strengthens the overall benefits package, and demonstrates that the organization understands employee wellbeing in practical terms rather than only through policy language.

Visit www.smartheritance.com or contact info@smartheritance.com to set up your family’s continuity record or explore how SmartHeritance fits into your benefits portfolio.

References

- DK Law Group (February 2026). Americans value personal digital assets at over $190,000 on average. dklawmd.com

- NordPass (2024). Average person manages 168 personal passwords. nordpass.com

- Family Business Association (January 2025). Less than 3% of adults have a digital estate plan. familybusinessassociation.org

- SavingAdvice.com (September 2025). Could Your Password Manager Be the Weak Link in Your Estate Plan? savingadvice.com

- BenefitsPro (April 2025). Digital estate planning becomes the new must-have employee benefit. benefitspro.com