80% of high-net-worth individuals have at least one form of digital wealth that is not included in their estate plan.

Not people who haven’t started planning. People who already have a will. A trust. A financial advisor they meet with regularly. People who have done every responsible thing that estate planning has ever asked of them, and still have a gap sitting quietly in the middle of everything they’ve built.

Here is the question that gap creates: if something happened to you today, could your spouse find and access everything your family needs within 48 hours? Not legally inherit it eventually, after months of paperwork and attorney calls. Actually find it, log into it, and know it existed in the first place.

For most households that have reached genuine financial complexity, the honest answer to that question is more uncomfortable than it should be. Not because of careless planning, but because the tools most families rely on were each built to solve a different problem. None of them were built for this one.

That is what a Personal Legacy Manager exists to fix.

When a Good Plan Isn’t Enough

Consider a scenario that plays out quietly in households all over the country.

Mark is a 47-year-old senior manager at a healthcare technology company in Chicago. He and his wife Sarah have two teenagers approaching college. Their combined household income is well into six figures. They have a will, a revocable trust, a financial advisor they see twice a year, three insurance policies, a 401(k) through his current employer, a Roth IRA, a taxable brokerage account at Fidelity, and an old 401(k) from a company he left in 2018 that he keeps meaning to roll over. He manages the household finances. Sarah trusts him to handle it.

Last spring, Mark traveled internationally for two weeks. On day four, a mortgage refinancing inquiry came in that needed a specific document from their trust. Then an insurance claim arrived that required a policy number neither Sarah could locate. Then a tuition payment portal sent an alert about a credit card on file that was about to expire and needed updating before a payment deadline.

She knew the Google Drive folder existed. She didn’t know which subfolder held which document. She knew he used a password manager. She didn’t have the master password. She knew they had insurance coverage. She couldn’t name the carriers or find the policy numbers.

Mark was eventually reachable after a delay in time zones. Nothing went seriously wrong. But they both came away from that two-week trip with a quiet, uncomfortable realization. They had planned well for the legal realities of their financial lives. They had not built anything that their family could actually operate without Mark there to explain it.

This is not a story about a family that failed at planning. It is a story about the gap that exists between a plan being legally sound and a plan being practically executable. Those are two different things, and most estate planning tools only address the first one.

According to research from the Wealth Management Institute, 80% of high-net-worth individuals have at least one form of digital wealth not captured in their estate plan. The National Association of Unclaimed Property Administrators reports that more than $77 billion in assets sit unclaimed across the United States right now, not because families lacked wealth, but because they lacked access to it when it mattered most. The average probate process lasts 18 to 24 months and can consume between 3% and 7% of an estate’s total value in legal fees, much of that driven by delays caused by missing documentation and inaccessible accounts.

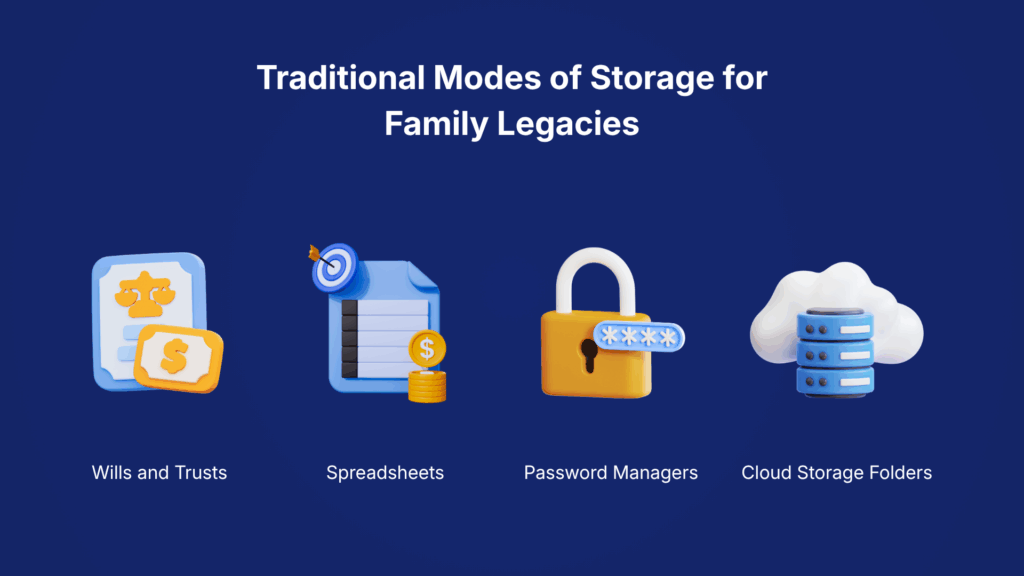

The tools most families rely on, including wills, spreadsheets, password managers, and shared cloud folders, each solve a piece of this problem. None of them solve the whole thing. That is the problem a Personal Legacy Manager was built to fix.

What Is a Personal Legacy Manager?

A Personal Legacy Manager is a secure digital platform that helps individuals organize all their financial accounts, digital assets, insurance policies, passwords, legal documents, and personal instructions in one place. It keeps this information continuously updated over time and ensures it reaches the right people, whether a spouse, adult children, or designated beneficiaries, at the right time, either during an emergency or after death.

Unlike a will, which defines legal distribution, or a password manager, which stores login credentials for daily use, a Personal Legacy Manager covers the complete picture: what you own, where it is, who should receive it, and how they access it when they actually need to.

You may have also come across the related term “digital legacy manager.” The two describe the same category of tool, but they are not identical in scope.

Digital legacy management, as practiced by platforms like DGLegacy, Everplans, and Clocr, typically focuses on the online layer: passwords, social media profiles, email accounts, and cryptocurrency wallets. The emphasis is on digital accounts specifically. A Personal Legacy Manager goes further. It covers the complete financial and personal picture, including insurance policies across all carriers, physical property, legal documents, personal instructions, final wishes, and the operational details that no legal document was ever designed to capture.

Think of it this way: a digital legacy manager helps your family access your accounts. A Personal Legacy Manager helps your family navigate your entire life. The difference is not a small one for anyone whose financial complexity has grown beyond a single bank account and a savings bond.

The global digital legacy market is projected to grow from $23 billion in 2025 to over $43 billion by 2030, a growth rate that reflects how quickly people are recognizing the gap between what traditional estate planning covers and what modern financial lives actually require. The Personal Legacy Manager is where that recognition becomes a system.

The Four Things That Fail When a Family Needs Them Most

Most families discover the real gaps in their planning not during a quiet planning conversation, but during a crisis, when discovering an account takes weeks, when a password no longer works, when nobody can find the document the attorney needs, or when a family realizes that an insurance policy existed but nobody can prove it.

Understanding where each commonly used tool stops is the only way to understand what a Personal Legacy Manager actually adds.

What a Will or Trust Does Not Cover

A will defines who inherits your property. A trust goes further, allowing assets to transfer outside of probate and providing more control over timing and conditions of distribution. Both create the legal authority needed for your wishes to be carried out. This legal foundation matters enormously, and nobody is suggesting otherwise.

But a will says who gets what. It does not say where things are, how to access them, or what credentials are needed to do so.

If you have a trust, it almost certainly includes a Schedule A, the document that lists the specific assets under the trust’s control. Schedule A is written at the time you sign the trust. Then life continues. You open a new brokerage account. You close an old savings account you no longer use. You acquire cryptocurrency. You switch life insurance carriers for a better rate. You open a Health Savings Account. Unless you return to your estate attorney and pay to update Schedule A each time something changes, which most people never do, the document quietly falls behind your actual financial life.

An outdated Schedule A does not simply leave gaps. It can actively cause confusion, delays, and missed inheritances. The legal system honors what is written. If an asset is not listed, it is not covered. And for someone managing a household with a net worth between $1 million and $20 million across multiple accounts and asset classes, the gap between what Schedule A says and what actually exists can be substantial.

Only 31% of Americans have a will at all. Among those who do, the vast majority have not updated it since a significant financial change in their lives. Among those with trusts, the majority have a Schedule A that is at least partially outdated. The legal layer is necessary. It is not sufficient.

When was the last time you updated yours?

What a Spreadsheet or Shared Document Cannot Do

Building a spreadsheet to track accounts, passwords, and important documents is a thoughtful instinct, and among financially organized households it is genuinely common. It represents real effort. For a while, it works.

The problem is that a spreadsheet captures life at one moment and then freezes there. Life does not freeze.

Passwords change, and the spreadsheet does not update. Accounts open and close. The spreadsheet sits in a folder on a laptop that no one else can unlock, or gets buried underneath hundreds of other files in a shared drive, or gets overwritten during a computer migration by an older version. There is no encryption protecting the credentials it contains, no controlled sharing mechanism to ensure only the right people see what they should, no beneficiary management, and no process to deliver the right information to the right person at the right time.

More importantly, a spreadsheet depends entirely on the person who built it to be accessible when it is needed. Most spreadsheet-based systems work perfectly for their creator. They fall apart the moment someone else needs to navigate them without guidance.

The real question is never whether the spreadsheet was well-built. It is whether your family knows it exists, knows exactly where it is, knows how to interpret what they find, and can access it without your help. If the answer to any of those is uncertain, the system fails at the exact moment it was designed to work.

What a Password Manager Was Not Built to Do

If you use 1Password, LastPass, or Bitwarden, you understand the value it provides for daily security. Strong, unique passwords for every account. Autofill across devices. Everything protected behind one master credential that only you know.

That last part is also the problem.

Password managers were designed for personal security during your lifetime. They were not designed for legacy transition, and these are fundamentally different problems requiring fundamentally different tools.

A password manager does not organize your financial life by asset category, beneficiary, or account type in a way that is interpretable by someone who did not create it. It stores credentials alphabetically or in whatever folders you set up. It does not track which insurance policy belongs to which carrier, or which brokerage account has which beneficiary designation, or what the account number is for the retirement plan you left at a previous employer. It does not include instructions, personal messages, or legal documents. It does not automatically notify anyone or trigger any process when you die.

When your family needs access after you are gone, they face a sealed vault that requires the master password, two-factor authentication through a device only you controlled, and navigation of an unfamiliar platform, all of this in a crisis, while grieving, under time pressure.

Some password managers have introduced emergency access features in recent years, allowing a designated contact to request access after a waiting period. This is a genuine improvement. It still requires that you have set it up in advance, that the designated person knows the feature exists, that they know how to initiate the request, and that they can navigate the interface once access is granted. Research from financial planning communities consistently shows that most users of these emergency features have not completed the setup, or have set it up with a contact who does not know it exists.

A password manager is essential for daily credential security. It was not designed for the transition your family faces when you are gone.

What a Cloud Folder Does Not Organize

Google Drive, Dropbox, and similar platforms make it easy to upload documents and share access with trusted people. Many families use them for exactly this purpose, and the intent is genuinely good.

The problem is that a cloud folder does not tell you what to put in it, does not ensure you update it when your life changes, and does not have any mechanism to deliver its contents to the right people at the right time.

There are no guided prompts for what a complete picture requires. There is no structured organization for different categories of assets and documents. There are no automated reminders to update when you open a new account or change an insurance carrier. There is no beneficiary management, no timed release, and no verified process for sharing. Files accumulate under inconsistent names, in nested folders that made sense at the time they were created and make no sense to anyone else, and often contain outdated versions alongside current ones with no obvious way to distinguish them.

Access depends entirely on someone knowing the account password, knowing the relevant folder exists, and knowing what they are looking for inside it. In the moments when this information would be most needed, none of those things are guaranteed.

What a Personal Legacy Manager Actually Does

A Personal Legacy Manager solves the problem that none of the tools above were designed to address: making sure your family can find, access, and act on your complete financial and personal picture, without months of searching, without missing assets, and without needing you there to explain a system you built.

It combines the best of what those tools attempt individually into one purpose-built system that was designed specifically for the transition your family will eventually face.

- A complete asset inventory that covers everything: Financial accounts, real estate, vehicles, insurance policies across all carriers, digital assets including cryptocurrency and domain names, subscriptions and memberships, and personal property with designated recipients. Not just the obvious accounts, but the ones you have accumulated over a twenty-year career that have quietly multiplied in the background.

- Credential storage is organized by asset category, not alphabetically: Usernames, passwords, PINs, security questions, and two-factor authentication details, structured so that someone navigating your financial life for the first time can find what they need without scrolling through a list of 168 unrelated entries.

- Beneficiary management that reflects your actual intentions: Your spouse receives what is relevant to managing the household immediately. Your adult children receive what they need to handle their portion of the inheritance. Your estate attorney receives what they need to execute the legal transfer. Not everyone needs access to everything, and a Personal Legacy Manager lets you assign the right information to the right people, which is something no will, spreadsheet, or password manager was designed to do with this level of precision.

- Document storage for everything that matters legally and practically: Wills, trusts, powers of attorney, healthcare directives, property deeds, vehicle titles, birth certificates, and tax returns, all in one organized place, not distributed across filing cabinets, attorney offices, and folders only you can navigate.

- Personal instructions and messages that legal documents cannot hold: Funeral preferences. Pet care instructions. Notes about which possessions carry particular sentimental weight and who should receive them. A message to your children that explains the decisions you made and the values behind them. A will cannot hold these things. A Personal Legacy Manager can.

- A system that updates continuously, not at one frozen moment: This is what distinguishes a Personal Legacy Manager from every other approach. Automated account discovery finds accounts you may have forgotten. Periodic update reminders keep the picture accurate as your financial life evolves. The record reflects your life as it is today, not as it was three years ago when you last sat down to maintain it.

- Timed, verified release that does not depend on anyone remembering to act: Your information remains completely private during your lifetime. It reaches your designated people through a verified process, not a shared password, not a folder link, but an automated confirmation mechanism that triggers the right delivery at the right time without requiring anyone to initiate an action they may not know to take.

This last point is what makes a Personal Legacy Manager fundamentally different from anything else on this list. A spreadsheet needs you to explain it. A password manager needs someone to know the master password. A cloud folder needs someone to know it exists. A Personal Legacy Manager needs none of these things. It works without you.

How many of your accounts could your family find right now without your help? Start organizing them for free with SmartHeritance.

Why Modern Households Need This More Than Any Previous Generation

In previous generations, a typical household’s financial life could fit in a single filing cabinet: one bank, one mortgage, a pension, a handful of account numbers, and a safe deposit box key. The map was simple enough that any organized adult could navigate it with an afternoon and a death certificate.

Today’s household looks nothing like that.

Consider what a typical 45-year-old professional with a household income above $100,000 actually manages. Multiple checking and savings accounts across two or three banks. An employer-sponsored 401(k). A Roth IRA opened during a different job. A taxable brokerage account at Fidelity or Schwab that holds individual stocks, index funds, and perhaps some options. An old 401(k) from a company they left in 2018 that hasn’t been rolled over yet. Two or three life insurance policies from different periods of their life. A mortgage. Perhaps a home equity line of credit. A 529 plan for each child. Cryptocurrency holdings in a hardware wallet or on an exchange. A Health Savings Account. Multiple credit cards with rewards programs and auto-pay setups. Dozens of subscriptions billed monthly across streaming services, software tools, and membership platforms. Social media accounts, cloud storage holding irreplaceable family photos, email accounts that serve as the recovery address for most of the above, and a password manager that holds credentials for all of it, protected behind a master password only one person knows.

According to NordPass research, the average person now manages 168 personal online accounts. That is 168 separate access points that a will says nothing about. For high-income households with longer financial histories and more complex asset portfolios, the real number is often higher.

Each of these elements is manageable on its own. Together, they form a map that typically exists in the head of one person in the household. According to research cited in SmartHeritance’s own data, roughly 50% of families rely on one spouse to manage day-to-day finances. When that person is suddenly gone, or even temporarily unreachable, the map disappears with them.

This is not a failure of planning. It is a structural gap in the planning tools that the financial and legal industries have made available. Wills were designed for a world where financial lives were simpler. Password managers were designed for a world where individual account security was the primary concern. Spreadsheets were designed for a world where manual updating was feasible. None of them were designed for the world that most financially complex households are actually living in now.

Who This Is For And the Specific Situations Where It Matters

You do not need to be disorganized to need a Personal Legacy Manager. You need to be honest about whether the financial life you have built over the past twenty years exists anywhere your family could navigate without you.

The clearest signal is not age or wealth in absolute terms. It is the ratio between the complexity of your financial life and the accessibility of that picture to the people who depend on it.

- The household where one person manages the finances. This is the most common configuration in American households, and it creates a quiet but significant risk. The person managing the finances knows which brokerage account holds what, which insurance policy covers which scenario, which autopay is coming out of which account. Their spouse trusts them completely. What the spouse does not have is the map. Research consistently shows that in households where one spouse manages finances, the other often cannot name all the accounts that exist, let alone access them quickly. The day the managing spouse is suddenly unreachable, for any reason, the map disappears.

- The executive or senior professional with accumulated financial complexity: Twenty years of career growth means twenty years of accounts, policies, investment platforms, and retirement plans accumulating across multiple employers and institutions. The old 401(k) from 2018 that hasn’t been rolled over. The insurance policy taken out during a different life stage. The Roth IRA opened at a brokerage that has since been acquired by another firm and renamed twice. Some of this even the primary account holder has half-forgotten. None of it is organized in a way that someone encountering it for the first time could interpret under pressure.

- The couple who has done everything their estate attorney asked: Will, trust, beneficiary designations updated, life insurance in force, financial advisor in place. They have genuinely checked every box that formal estate planning offers. The gap is not in the legal framework. It is in the operational layer that sits between a legally sound plan and a practically executable one. Their beneficiaries are correctly named. Whether those beneficiaries can locate the accounts those designations are attached to, without a guided system to help them, is a separate question that the legal documents do not answer.

- The person who recently spent months untangling a parent’s estate: They called banks that required death certificates, letters testamentary, and notarized affidavits before they would confirm an account even existed. They found savings accounts by searching through old bank statements. They discovered a life insurance policy only because a monthly debit appeared on a credit card statement. They spent months navigating a process that compounded grief with administrative exhaustion. They finished with a quiet determination not to put their own family through the same thing, and have not yet done anything about it.

- The business owner with intertwined personal and business finances: Personal and business accounts at the same bank. Business credit cards with personal guarantees. Business insurance that affects personal liability. Ownership stakes that require specific documentation to transfer. For business owners, the operational gap in estate planning is even more significant because the stakes of a delayed or disorganized transition extend beyond the family to employees, clients, and business partners.

A Personal Legacy Manager is not a product for people who have not started planning. It is what comes after you have done the legal work, the practical layer that turns a legally sound estate plan into one your family can actually use.

See how SmartHeritance works as a Personal Legacy Manager for households like yours. Take a free guided tour.

What a Complete Personal Legacy Manager Should Include

If you are evaluating whether a tool genuinely qualifies, or whether what you currently have is sufficient, here is the full inventory of what a complete Personal Legacy Manager should cover. Most people find gaps in at least two or three of these areas when they look at their current systems honestly.

- A full asset inventory that goes beyond financial accounts: This means every financial account across every institution, organized by type and institution. It also means insurance policies across all carriers, including life, disability, long-term care, and any riders. Real estate, including deeds and mortgage details. Vehicles with titles. Digital assets including cryptocurrency wallets, NFTs, and domain names. Recurring subscriptions and memberships that carry real financial weight, because a family suddenly responsible for managing finances needs to know what is auto-billing and from which account. And personal property with specific designated recipients for items that carry sentimental value beyond financial worth.

- Credential storage organized by account category: Not an alphabetical list of login credentials, but a structured record organized by the type of account and the institution holding it, so that someone navigating your financial life for the first time can find the Fidelity login when they are looking for the Fidelity account, not when they happen to scroll past it. This means usernames, passwords, PINs, security questions, and two-factor authentication details, including information about which phone number or authenticator app is linked to which account.

- Beneficiary assignment with granular precision: Different people in your life need different information at different times. Your spouse needs immediate access to household accounts, insurance policies, and ongoing financial obligations. Your adult children need access to their portion of the inheritance. Your estate attorney needs access to legal documents. Your financial advisor needs access to investment account details. A Personal Legacy Manager lets you assign the right information to the right people, so that each person receives exactly what is relevant to their role, and nothing they do not need.

- Legal document storage that is actually accessible: Wills, trusts, powers of attorney, healthcare directives, advance directives, property deeds, vehicle titles, birth certificates, marriage certificates, Social Security cards, and recent tax returns. These documents are most needed during a crisis, which is precisely when a filing cabinet, a banker’s box in the back of a closet, or a folder at an attorney’s office is least convenient. A Personal Legacy Manager stores them digitally, organized, and accessible to the right people when they are needed.

- Personal instructions and messages that belong nowhere else: Funeral and burial preferences, including specific wishes your family may not know to ask about. Pet care instructions and veterinary contacts. Notes about possessions that carry particular sentimental meaning. Instructions for managing ongoing household obligations in the immediate aftermath of a death. And personal messages to your spouse, your children, or other people you love, the kind that do not belong in a legal document but that matter enormously to the people you are trying to care for. A will cannot hold these. A Personal Legacy Manager can.

- A record that updates continuously rather than freezing at one moment. This is the operational failure of every alternative system. A will updates when you pay an attorney to update it. A spreadsheet updates when you remember to open it. A cloud folder updates when you are organized enough to maintain it consistently over years. A Personal Legacy Manager uses automated account discovery to surface accounts you may have forgotten and sends periodic update reminders that prompt you to review and confirm that your record reflects your actual financial life. The record stays current because the system is designed to keep it current, not because of your personal discipline.

- Timed, verified release that works without human intervention. This is what separates a Personal Legacy Manager from every other approach on this list. Your information stays completely private during your lifetime. Nobody can see it unless you choose to share it. When a verified event is confirmed, whether a period of inactivity, a wellness check that goes unanswered, or a confirmed death, the system automatically delivers the right information to the right people without requiring anyone to initiate an action they may not know to take. No one needs to find a folder. No one needs to guess a password. No one needs to remember that a system exists and know how to operate it under the worst circumstances of their lives.

How a Personal Legacy Manager Is Different From a Digital Legacy Manager

This distinction comes up often enough that it deserves a dedicated explanation, because the two terms are used interchangeably in some contexts and the difference matters for someone trying to understand what they actually need.

A digital legacy manager, as the term is used in most market contexts and by most competing platforms, focuses on the digital layer of someone’s life: their online accounts, passwords, social media profiles, email access, and cryptocurrency holdings. The core problem it solves is account access: making sure someone can log in to the accounts that only the deceased knew how to access.

This is a real and important problem. The average person manages 168 online accounts, and a family without access to those credentials faces a slow, frustrating process of contacting individual platforms with death certificates and legal documentation, often discovering that many platforms have no formal process for account access by survivors at all.

But digital account access is one layer of a much larger problem.

A Personal Legacy Manager covers that digital layer and then extends to the complete picture of someone’s financial and personal life. Insurance policies that exist on paper or in email confirmations but are not part of any digital account system. Physical assets, including real estate, vehicles, and personal property, that have no online login. Legal documents that define authority and distribution but need to be findable by the right people at the right time. Personal instructions and messages that belong in no legal document. Professional contacts, including the names of the estate attorney, the financial advisor, the accountant, and the insurance agent, with the context needed to know why each one matters.

The simplest way to think about it: a digital legacy manager helps your family access your accounts. A Personal Legacy Manager helps your family navigate your entire life, including everything that exists beyond a login screen.

For someone managing the kind of financial complexity that comes with a household income above $100,000 and a net worth built over decades, the gap between these two scopes is the difference between a partial solution and a complete one.

The Privacy Question Most People Ask Before They Start

Before anyone commits to storing the most sensitive details of their financial life in any system, the first question they ask is whether it is safe. This is the right question, and it deserves a direct answer rather than marketing language.

SmartHeritance uses AES-256 encryption, which is the same standard used by financial institutions and government agencies, to protect data both at rest and in transit. This means that even in the event of a security breach at the infrastructure level, the encrypted data would be computationally unreadable without the proper keys.

SmartHeritance is Google CASA Tier 2 certified, which means it has been independently validated against Google’s Cloud Application Security Assessment framework, one of the more rigorous third-party security standards available to consumer software companies.

SmartHeritance uses a zero-knowledge architecture. This means the platform is technically designed so that no SmartHeritance employee can read, view, or access your personal data under any circumstances, including a legal request, a security audit, or internal troubleshooting. Only you and the people you explicitly designate can ever see what you have stored. This is not a policy commitment. It is a technical constraint built into how the system works.

Role-based access control ensures that even within the platform, different types of data are accessible only to the categories of users you have specified. Your spouse sees what you have designated for your spouse. Your adult children see what you have designated for them. No one sees anything you have not explicitly assigned to them.

Your data belongs to you and can be exported at any time. It is not locked inside a proprietary system with no exit path. If you ever choose to leave the platform, your information comes with you.

How SmartHeritance Works as a Personal Legacy Manager

SmartHeritance was built specifically as a Personal Legacy Manager for households at the stage where financial complexity has outpaced the organizational tools available to manage it.

Here is how it addresses each of the gaps that wills, spreadsheets, password managers, and cloud folders leave open.

Your will does not know your passwords. The SmartHeritance Comprehensive Digital Vault stores all your accounts, credentials, policies, and documents in one secure, encrypted place. Adding or updating anything takes minutes and requires no attorney.

Your asset list is outdated. SmartSync, which is patent-pending, automatically scans your email for financial account confirmations, insurance notices, subscription receipts, and other signals that surface accounts you may have forgotten or acquired since the last time you deliberately organized your financial picture. Your record stays current without requiring you to remember to maintain it manually.

Spreadsheets break down when the person who built them is gone. SmartHeritance is organized by category and role, so that a family member navigating your financial life for the first time has a structured system to work with, not a personally organized filing system that only makes sense to its creator.

One person holding all the information is a single point of failure. The Wellness Protocol monitors your activity and automatically initiates a release process when extended inactivity is detected. If you are active, nothing happens. If you do not respond to a check-in within the protocol window, the system confirms with a designated successor before releasing information to your designated beneficiaries. No single person needs to hold everything. No one needs to remember that the system exists and know how to operate it at a moment of crisis.

Families spend months searching for what should take days. Your loved ones receive organized, categorized access to exactly what they need, with the context to understand what they are looking at and what to do with it.

Setup takes less than 15 minutes. Plans start at $2.99 per month, which is less than a single cup of coffee. There is a free trial available with no credit card required. SmartHeritance is SOC2 compliant and Google CASA Tier 2 certified.

“Finally, there is peace of mind regarding the loss of assets and what might happen if an unforeseen accident occurs.” — Venky, Small Business Owner, Los Angeles”

“The wellness and personalized checks give me peace of mind to know that if something does happen, my family will receive all of the information they need.” — Adam, Product Executive, Chicago”

“I’m incredibly grateful for SmartHeritance. It gives me peace of mind knowing that if I were to pass away unexpectedly, my loved ones would have all the information they need. The platform is intuitive, user-friendly and made it easy to get started in no time.” — Mamata, Software Consultant, Columbus, OH”

If you already have a will and a trust, SmartHeritance completes the picture they leave open. If your Schedule A has not been updated since you signed your trust, SmartHeritance builds the living record that fills the gap your legal documents were never designed to address.

Start for Free. No Credit Card Needed. Take a Guided Tour.

Frequently Asked Questions

-

Is a Personal Legacy Manager the same as estate planning?

No. Estate planning is the legal layer. It defines who inherits your assets. A Personal Legacy Manager is the operational layer. It ensures your family can actually find and access those assets. Your will tells them who gets what. A Personal Legacy Manager tells them where everything is and how to reach it.

-

I already have a password manager. Why isn’t that enough?

A password manager stores credentials for your own daily use. It does not organize assets by type or beneficiary, does not include legal documents or personal instructions, and has no process to release information to your family after your death. It also requires them to know the master password and navigate an unfamiliar tool during a crisis. These are different problems that require different tools.

-

I already have a will. Do I need this too?

Yes. A will defines who receives your assets. It says almost nothing about where those assets are, how to access them, or what credentials are needed. A Personal Legacy Manager handles the practical access layer your will was never designed to address. The two work together.

-

Is my data safe in a Personal Legacy Manager?

SmartHeritance uses AES-256 encryption and a zero-knowledge architecture, meaning not even SmartHeritance employees can view your data. It is Google CASA Tier 2 certified and SOC2 compliant. Only you and the people you designate can ever access what you store.

-

How is a Personal Legacy Manager different from a shared Google Drive folder?

A cloud folder stores files. A Personal Legacy Manager organizes them with guided structure, automated update prompts, beneficiary-level access controls, and a verified release mechanism. Uploading documents to a shared folder and hoping your family finds them in a crisis is storage. A Personal Legacy Manager is a system.

-

How often should I update my Personal Legacy Manager?

SmartSync handles much of this automatically by surfacing forgotten accounts and sending update reminders. As a rule, review after any significant financial change: a new account, a policy switch, a property transaction, or a major life event. At minimum, a full review once a year keeps everything accurate.