TL;DR

- Most families are not unprepared because they lack assets. They are unprepared because nobody knows where anything is.

- Family continuity planning is the organized, current, accessible record of your financial, digital, legal, and personal information, paired with a mechanism that delivers it to your family when something happens. It is not estate planning. It is the operational layer that makes estate planning work.

- Settling an estate without organized records requires an average of 570 hours of executor work over 16 months, time that lands entirely on grieving family members.

- The NAIC’s Life Insurance Policy Locator has connected families with $13.18 billion in unclaimed benefits from policies that were active and paid for but could not be found. A continuity plan prevents this.

- A will, a life insurance policy, and a financial advisor each solve a different problem. None of them solves the discoverability problem. That is what this article covers.

- Use the eight-element framework below as your starting checklist, and use SmartSync to build it without doing the work manually.

This scenario plays out often enough that estate attorneys and financial advisors have seen a version of it in nearly every practice: a parent dies, and the adult children who thought everything was handled discover that handled and organized are two completely different things.

A father dies unexpectedly at 68. He has a will, life insurance, and a financial advisor he has trusted for years. What he does not have is any organized record of where any of it lives. His son spends the next eight months calling financial institutions, tracking down an insurance policy through an agent who has since retired, and eventually discovering a 401(k) from a job his father left in 2004 that nobody in the family had known existed.

The will was clear. The estate was not. That gap between what legal documents describe and what families can actually find and act on is what family continuity planning addresses.

What Family Continuity Planning Actually Means

Family continuity planning is the deliberate organization of a household’s financial, digital, legal, and personal information so that trusted family members have what they need, and know where to find it, when a death, illness, or sudden incapacity occurs.

It is not estate planning. Estate planning creates the legal instruments (wills, trusts, powers of attorney) that govern what happens to your assets. Family continuity planning creates the operational record that makes those instruments findable and actionable. One describes what your family receives. The other ensures they can locate it.

It is also not a digital vault or a document folder. Those store things. Family continuity planning is a living system that stays current as your financial life changes and includes a mechanism that ensures your family actually receives the information when they need it.

SmartHeritance is built specifically for this: a Family Continuity Planning platform that helps individuals organize, maintain, and deliver the information their families will need, without requiring a manual update every time something in their financial life changes.

Why a Will, Insurance, and a Password Manager Are Not Enough

The most common reason families do not have a continuity plan is that they believe they already do. A will, life insurance, a financial advisor: each of these addresses a real and important problem. None of them addresses the operational problem of discoverability.

A will describes distribution, not discoverability

A will tells your family who receives your assets. It does not tell them which accounts exist, which institutions hold them, or what they need to begin the process of claiming anything. The executor has legal authority the moment probate opens, but legal authority and organized information are entirely different things. Without the latter, that authority gets spent making phone calls and waiting on records that may take months to arrive.

Life insurance pays out, but families have to find it first

The NAIC’s Life Insurance Policy Locator has connected families with more than $13.18 billion in unclaimed life insurance benefits through August 2025, across more than 611,000 matched requests. These are policies that were paid for, maintained, and active, and went unclaimed because the family did not know they existed or could not locate the policy number. Life insurance provides the financial protection a policyholder intended. A continuity plan ensures that protection can actually be accessed.

A password manager covers credentials, not the full map

Password managers protect against unauthorized access while you are alive. They were not built for inheritance. Most require a master password a surviving family member may not know, and many require two-factor authentication tied to a device the family cannot access. Beyond that, they only cover accounts the user already knows about. They do not surface the retirement account from a previous employer, the digital wallet on an old email address, or the investment account opened years ago and never mentioned to anyone.

Estate planning vs. family continuity planning, side by side:

| Estate Planning | Family Continuity Planning | |

| What it creates | Legal instruments (will, trust, POA) | An organized, accessible record |

| What it describes | Who receives what | What exists and where it is |

| Who produces it | Attorney-led | Self-organized with platform support |

| When it matters | At legal distribution | At the moment of crisis |

| Whether it stays current | Rarely updated | Designed to stay current |

| Whether family can act on it alone | Often not, they still need the map | Yes, the map is the product |

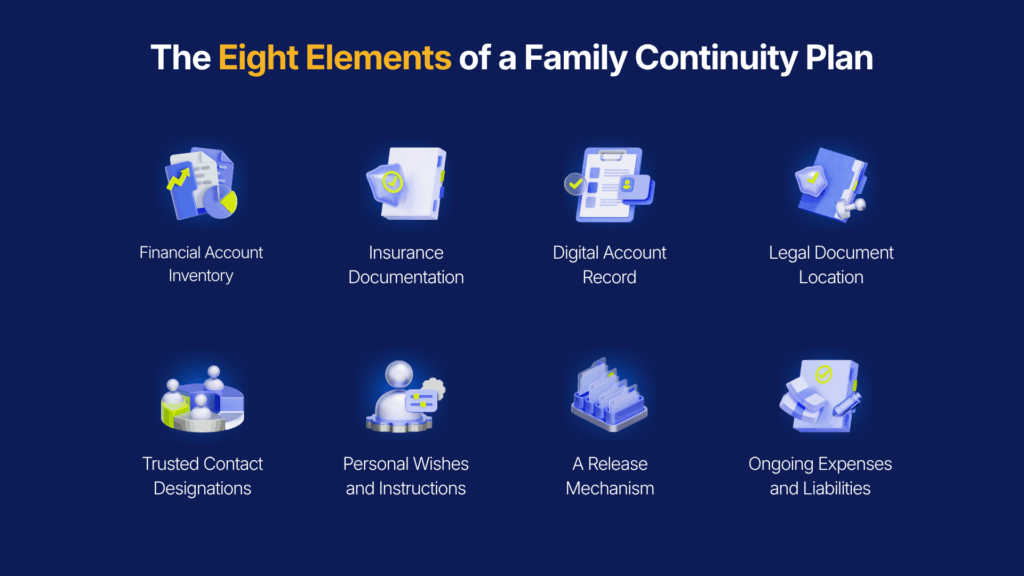

The Eight Elements of a Family Continuity Plan

A family continuity plan covers eight categories. Each one addresses a specific point where families hit dead ends when navigating an estate without organized information.

- Financial Account Inventory: A record of every bank account, investment account, retirement fund, and brokerage with institution names, account types, and contact information. Without it, families spend months contacting institutions they discover through old paper statements.

- Insurance Documentation: Life, health, disability, and long-term care policies with policy numbers, carrier names, and beneficiary designations. The $13.18 billion in unclaimed life insurance is a documentation gap, not a database error. Families could not find the policy when they needed it.

- Digital Account Record: Online accounts with financial significance including digital wallets, cryptocurrency platforms, investment apps, and subscription services still charging a card. According to NordPass’s 2024 research, the average person manages 168 passwords. Most of those accounts are ones a surviving family member would not know to look for.

- Legal Document Location and Storage: Where documents are held and, where possible, digital copies of the documents themselves. SmartHeritance allows users to store digital copies of their will, trust, power of attorney, and advance directives directly on the platform alongside location details for any originals held elsewhere.

- Trusted Contact Designations: A record of who receives what information and under what conditions. Attorney, financial advisor, insurance agent, family members, with current contact details and each person’s specific role. Without this, families spend the first weeks of estate administration just figuring out who to call.

- Ongoing Expenses and Liabilities: Mortgage, utilities, loan payments, and recurring subscriptions that continue accruing after a death. Without a current record, families discover these obligations only when accounts become delinquent or a subscription renews on a card nobody recognized.

- Personal Wishes and Instructions: Funeral preferences, guidance on sentimental assets, messages for family members, and context for decisions that legal documents do not address. These reduce the number of calls a family has to make under pressure.

- A Release Mechanism: The element most plans miss entirely. An organized record has no value if the family does not know a platform exists, cannot access it, or has to go to court to retrieve it. A release mechanism ensures information reaches the right people at the right time without the family having to initiate anything.

Why Continuity Plans Go Out of Date and How to Prevent It

Most continuity planning failures are not failures of intention. Someone builds a record, files it, and then life keeps moving. A new employer brings a new retirement account. A policy moves to a different carrier. A digital wallet gets set up for a service that did not exist three years ago. Each change is individually unremarkable. Collectively, they mean that a record accurate in 2022 can be significantly incomplete by 2025.

Manual maintenance asks people to update a document every time anything in their financial life changes. In practice, it does not happen. The record drifts invisibly until a family discovers the gap at the worst possible time.

SmartSync solves this by connecting to a user’s email and scanning for correspondence from financial institutions, insurance carriers, investment platforms, and subscription services. When a new account opens and generates a confirmation email, SmartSync identifies it. When a policy moves to a new carrier, SmartSync picks up the update. Personal emails are never accessed or stored. SmartSync only reads the financial and institutional correspondence trails that accounts generate by default.

How Your Family Actually Receives the Information

There is a category of continuity plan that fails completely despite being thorough: one stored somewhere the family does not know about, protected by credentials they cannot access, or dependent on a conversation that was planned but never happened. Having a plan your family cannot reach is functionally the same as having no plan.

If something happened to you today, how would your family know a continuity plan exists? Where would they find it? What happens if accessing it requires your phone for authentication?

The Wellness Check Protocol closes this gap. It monitors activity on the platform. If there is extended inactivity, it sends a check-in to the user. If the user confirms they are fine, the clock resets. If there is no response, the platform reaches out to designated family members. If those contacts confirm something has happened and provide verification, the platform releases the stored information to the designated recipients, the people the user chose, in the way they intended, without requiring the family to know the platform exists or to initiate any contact.

What Estate Administration Without a Continuity Plan Actually Costs

According to EstateExec’s national executor study, settling an estate requires an average of 570 hours of work over 16 months. That is not time spent grieving. That is the administrative work of locating accounts, contacting institutions, and navigating a financial life that was never organized for anyone else to use.

When an estate goes through probate, Trust & Will’s 2024 Probate Study found the average timeline is 20 months, and only 2% of Americans correctly guessed how long it takes. Most assume the process takes weeks. The same study found the average cost of probate is around $14,000, and that is before attorney fees on complex estates.

According to NAUPA, 1 in 7 Americans is owed some form of unclaimed property, and state programs returned $4.49 billion to rightful owners in fiscal year 2024 alone. That is only what was actively claimed. The rest remains in state custody indefinitely.

A December 2025 Homethrive survey of 1,000 full-time employees found that 45% of estate executors spent four or more hours per week on estate tasks during regular business hours. That work does not stop when bereavement leave ends.

Who Actually Needs a Family Continuity Plan

Family continuity planning is not a retirement activity and not exclusive to large estates. It applies to anyone whose family would struggle to locate their accounts, policies, and documents if something happened today. A few profiles that come up consistently in estate administration:

- The person in their 40s with a layered digital financial life: Multiple investment platforms, retirement accounts from previous employers, a digital wallet, a life insurance policy purchased through an agent three years ago, and subscriptions auto-renewing from accounts a spouse has never seen. They have more accounts than they could list from memory.

- The couple where one partner manages everything: One person knows every institution, account, and carrier. The other has a general sense and no specific knowledge of how to access anything. This arrangement is common. It is also a continuity risk that rarely gets named until it becomes a problem.

- The adult child watching a parent delay this conversation: The parent holds accounts and policies accumulated over decades. The adult child knows the conversation needs to happen but cannot figure out how to start it without it feeling like a conversation about death rather than a conversation about care.

- The executor who has already been through it: They spent over a year locating what their parent had built. They know exactly what that costs in time and stress. They do not want their own family to have the same experience.

How to Start Building One

A family continuity plan is not a document you create once and file. It is the ongoing work of keeping an organized, current, accessible record of your financial life and ensuring the right people can reach it when something happens.

Most people have a will, insurance, and a financial advisor. What they do not have is an answer to a simpler question: if something happened to you today, could your family find everything, access everything, and act on everything without you there to walk them through it?

The $13.18 billion in unclaimed life insurance recovered through the NAIC’s policy locator does not belong to families who did not love their people. It belongs to families whose people did not have a continuity plan.

SmartHeritance helps you build a complete continuity plan: organizing your financial, digital, legal, and personal information in one secure place (SmartHeritance is SOC 2 Type II compliant, independently audited across all operational and security standards), keeping it current through SmartSync’s automated account discovery, and delivering it to the right people through the Wellness Check Protocol when the time comes. When you sign up, you can connect your email and run SmartSync immediately to see which accounts you hold that your family does not know about. Start at www.smartheritance.com.

FAQ

-

How is family continuity planning different from legacy planning?

Legacy planning covers what you want to pass on. Family continuity planning ensures your family can actually find and access it when something happens.

-

What should I do first when a parent dies and I do not know where their accounts are?

Search the email inbox for bank statements, insurance notices, and investment summaries. Every financial account leaves a correspondence trail, and that trail is the fastest map to what exists.

-

What happens to digital accounts and online subscriptions when someone dies?

Subscriptions keep charging, platforms lock accounts, and cryptocurrency becomes permanently inaccessible without a private key. Without a documented record, most digital accounts are never found or properly closed.

-

How do I start a family continuity plan if I have no idea what accounts I hold?

Connect your email to SmartSync. It scans your inbox for financial correspondence and surfaces accounts you may have forgotten, giving you a starting inventory without manual effort.

-

Can a family continuity plan replace a will?

No. A will governs how assets are distributed. A continuity plan ensures your family can find those assets in the first place. Both are necessary and solve different problems.

-

How do I talk to my parents about organizing their financial information?

Frame it around reducing burden, not anticipating death. SmartHeritance’s Parent Account feature lets an adult child set up and maintain a parent’s continuity record on their behalf, so the conversation is about care, not loss.

References

- NAIC. Life Insurance Policy Locator Tool Helps Consumers Connect with More Than $13 Billion in Benefits, September 30, 2025. https://content.naic.org/article/naic-life-insurance-policy-locator-tool-helps-consumers-connect-more-13-billion-benefits

- EstateExec. National Executor Study (570 hours / 16 months data). https://www.estateexec.com/Docs/ExecutorStudy.pdf

- Trust & Will. The State of Probate in America, 2024 Probate Study, July 2024. https://trustandwill.com/learn/2024-probate-study

- Caring.com. 2024 Wills and Estate Planning Survey. https://www.caring.com/resources/2024-wills-survey

- NordPass. How Many Passwords Does the Average Person Have? May 2024. https://nordpass.com/blog/how-many-passwords-does-average-person-have/

- NAUPA. Unclaimed Property Day Returns Money to Americans, January 21, 2025. https://www.globenewswire.com/news-release/2025/01/21/3012848/0/en/Unclaimed-Property-Day-Returns-Money-to-Americans.html

- Homethrive. Survey Shows Minimal Support Post-Bereavement Leave, December 11, 2025. https://markets.financialcontent.com/lightport.lightport3/article/accwirecq-2025-12-11-survey-shows-minimal-support-post-bereavement-leave-creating-strain-on-employees-and-workplaces