TL;DR

Billions in unclaimed assets sit with US state governments every year, not because families were careless, but because no system existed to keep pace with a financial life that kept growing. This article explains:

- Why wills and password managers do not solve the hidden assets problem

- What causes accounts and policies to go missing after a death

- What a working estate organization system actually does to prevent it

The Scale of Unclaimed Property After Death in the United States

Consider what an adult child faces after a parent passes. They are standing in a house full of decades of accumulated financial life with no map for any of it:

- An insurance envelope with no company name on the front

- A bank statement from an institution nobody in the family recognizes

- A quarterly investment report from a brokerage account nobody knew existed

- A 401k from a job held twenty years ago at a company that has since been acquired twice

This does not happen because the parent failed to plan. In most versions of this story, there was a will, notes left somewhere, a general understanding between spouses. What was missing was not intention. It was a system capable of tracking a financial life as it actually grew.

The numbers that describe this gap are not edge cases. They are the predictable outcome of an infrastructure failure playing out in millions of households every year.

Unclaimed property held by US state governments:

- Approximately $70 billion total, belonging to roughly one in seven Americans, according to NAUPA

- New York State alone holds over $19 billion

- California holds approximately $15 billion

- Texas holds $10.5 billion

This money is not held because it was poorly managed. It is held because the families it belongs to do not know it exists.

Forgotten 401k accounts as of July 2025:

- 31.9 million forgotten accounts in the United States, per Capitalize and the Center for Retirement Research

- $2.13 trillion in combined assets

- Average forgotten account balance of $66,691

- 4 million accounts abandoned in 2024 alone, mostly from ordinary job changes, not death events

Life insurance benefits going unclaimed:

- The NAIC Life Insurance Policy Locator has matched consumers with more than $13 billion in life insurance and annuity benefits since 2016

- That tool exists because beneficiaries routinely have no idea a policy was ever in force

- A policy purchased specifically to protect a family sits unclaimed because nobody knew where to look

Across three distinct categories of assets, the same structural failure repeats itself. The money exists. The documentation exists somewhere. What is missing is a live, current record that connects the two.

Why a Modern Financial Life Cannot Be Tracked With a Single Document

Financial life does not stay still. It accumulates over decades, and every change creates a potential gap:

- Every job change potentially creates a new, forgotten retirement account

- Every insurance renewal is a new policy number, sometimes with a new provider

- Every platform joined and never revisited is a future search task for a grieving family

The US Bureau of Labor Statistics reported in September 2024 that median employee tenure fell to 3.9 years in January 2024, the lowest level since 2002. Workers born between 1957 and 1964 held an average of 12.4 jobs before age 54. Each of those job changes was a potential orphaned retirement account.

The average person today manages over 160 digital accounts across banks, brokerages, insurance portals, retirement platforms, cloud storage, and subscription services. No manual record keeps up with this without someone actively updating it after every change. And nobody does that consistently, because life does not pause to prompt the update.

Before building SmartHeritance, founder Pravat Lall spoke with roughly 70 to 80 families who had either handled a parent’s passing firsthand or watched someone close to them go through it. What those conversations consistently revealed was not that people had failed to try. Most had done something: a will, instructions left with a spouse, a folder somewhere. The failure was structural. The record did not keep up with the life.

Why a Will and a Password Manager Do Not Solve the Hidden Assets Problem

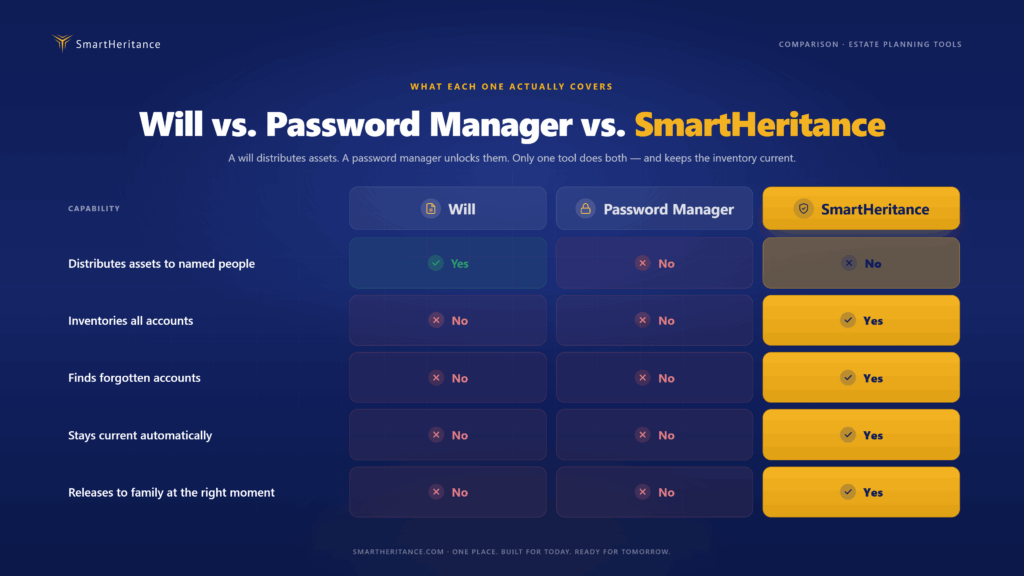

The will problem:

A will is a distribution document. It specifies who receives which assets after a death. What it does not do:

- Inventory those assets

- Identify where they are held

- Tell a family how to locate and access accounts

- Account for anything opened after the will was drafted

An executor acting on a will still has to find what the will distributes. If accounts were opened after the will was written, or were simply never listed, the will offers no guidance on where to start.

The password manager problem:

A password manager stores credentials for accounts a person actively manages and remembers to add. What it does not do:

- Find accounts opened before the password manager existed

- Surface accounts that were set up and forgotten

- Discover a retirement account from a job held fifteen years ago

- Release anything to the family in a verified, controlled way

If the master password is known only to the account holder, the password manager itself becomes another locked room the family is trying to enter at exactly the wrong time.

The gap between legal planning and operational readiness is precisely where decades of a person’s financial life can go missing. The assets are there. The legal framework may be there. The system for finding them is almost always absent.

How an Estate Organization System Keeps a Financial Record Current Across a Lifetime

Every financial account a person has ever opened has generated an email trail:

- Bank accounts send welcome emails and monthly statements

- Insurance policies send renewal correspondence and coverage summaries

- Retirement accounts send quarterly performance statements

- Brokerages send trade confirmations

- Subscription services send receipts

That existing correspondence trail is the raw material that makes automated account discovery possible, without requiring anyone to remember everything manually.

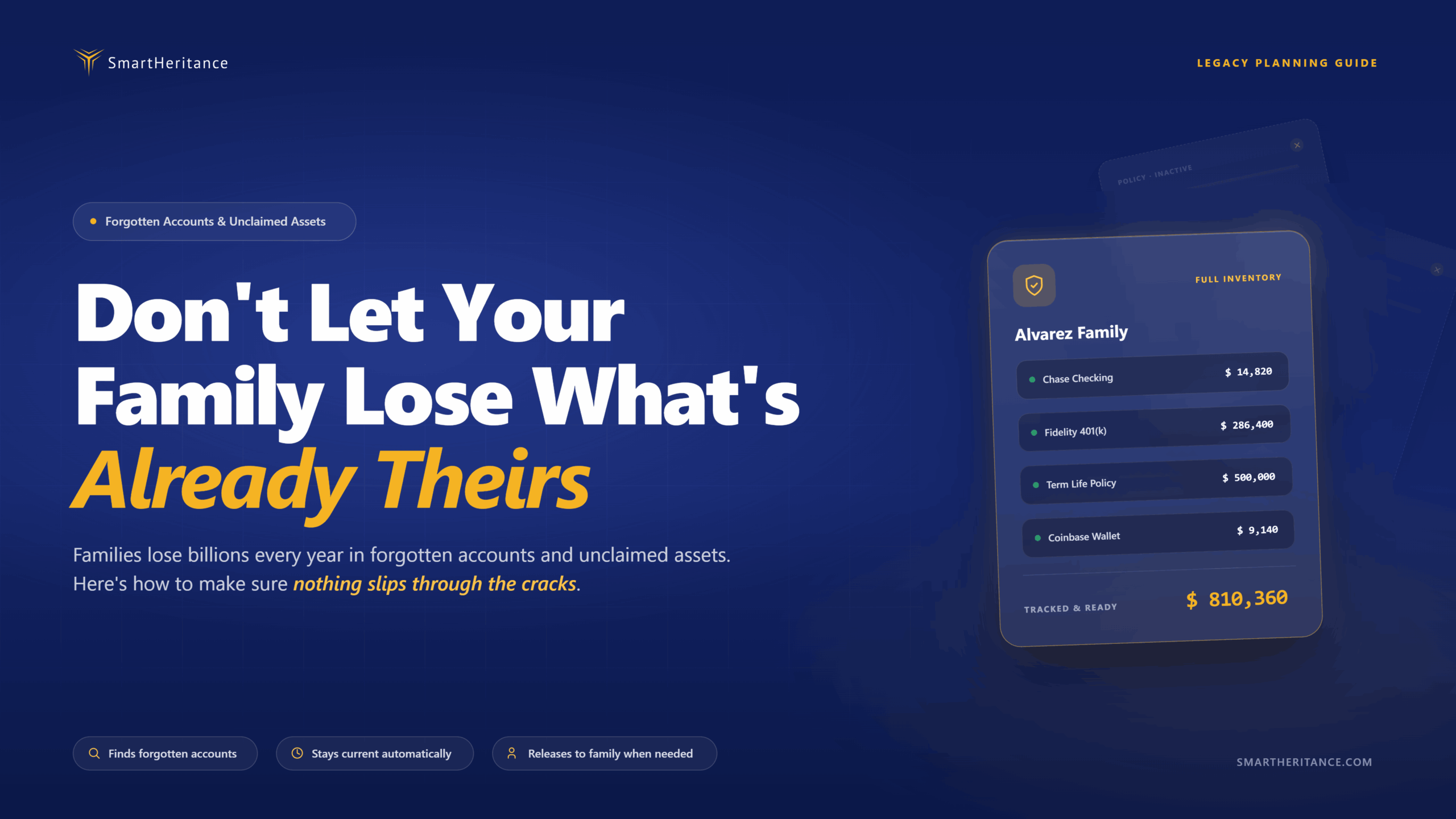

How SmartSync works:

SmartSync, SmartHeritance‘s account discovery feature, uses that email trail to build an organized record automatically:

- Connects to Gmail, Outlook, or Yahoo

- Scans for correspondence from over 100 financial institutions, brokerages, insurance providers, and retirement platforms

- Extracts account information and organizes it into structured records

- Presents everything to the user for review and approval before anything is stored

- Personal emails are never accessed or stored

For what does not come through email, such as property records and physical assets, SmartHeritance sends periodic prompts to add those details manually over time.

How the record stays current:

SmartSync does not run once and stop. It rescans every few months. When a new account is opened and a confirmation email arrives, SmartSync captures it on the next pass. The record stays current because the system keeps working, not because the user keeps remembering.

How the record reaches the family:

An organized record that the family cannot access at the right moment is no better than no record at all. SmartHeritance addresses this through the Wellness Check Protocol:

- Monitors account activity continuously

- Checks in directly with the user if there is prolonged inactivity

- Contacts designated family members if there is no response

- Releases the organized record only after a verified life event is confirmed through appropriate documentation

The family never has to search for a platform or remember that one exists. The information reaches them when it is needed.

The Real Cost of Leaving Assets Unorganized for Your Family

The administrative burden of an unorganized estate falls entirely on the people left behind, during the hardest period of their lives, while they are simultaneously:

- Managing grief

- Coordinating across family members

- Navigating legal and probate processes

- Maintaining their own professional and family responsibilities

Research from Empathy’s Cost of Dying reports suggests bereaved families spend approximately 20 hours per week for more than a year settling a loved one’s affairs. Most of that time is not legal or financial planning. It is administrative reconstruction: finding accounts, locating policies, and resolving access issues on platforms that were never designed with inheritance in mind.

The 4 million 401k accounts abandoned in 2024 are a reminder that this fragmentation is happening right now, not only after a death. Accounts opened and forgotten, policies renewed and misfiled, platforms joined and left behind: these accumulate into a continuity gap that widens every year without anyone actively widening it.

Addressing that gap before it becomes someone else’s burden is one of the most practical things a person can do for the people who depend on them.

How SmartHeritance Helps Families Organize Assets and Avoid the Unclaimed Property Problem

SmartHeritance is a Family Continuity Planning platform built around the two failures that appeared consistently across those family conversations: no system existed to keep the record current alongside a changing life, and when information did exist, the family had no reliable way to reach it.

What SmartHeritance does:

- Builds an organized record of financial, legal, personal, and digital information in one secure place

- Uses SmartSync to automatically discover accounts through existing email correspondence

- Keeps the record current through periodic rescans without manual input

- Releases the record to designated family members only after a verified life event is confirmed

- Stores everything in a zero-knowledge architecture vault where no one at SmartHeritance, including its own team, can see what a user has stored

- Encrypts all data at rest and in transit using AES-256 encryption

- Is independently validated through Google CASA Tier 2 certification

What SmartHeritance is not:

SmartHeritance is not estate planning software. It does not replace wills, trusts, or legal documents. It is the operational layer that makes whatever planning a family has already done findable and usable when the moment arrives, and that ensures the accounts, policies, and assets built over a lifetime do not become part of the $70 billion sitting unclaimed in state treasuries.

Start organizing your family’s continuity record at www.smartheritance.com

FAQS

How long do state governments hold unclaimed property before it is gone permanently?

Most states hold unclaimed property indefinitely, so there is no permanent deadline to claim it. Assets transfer to the state after one to five years of inactivity depending on the state and asset type.

What types of assets are most commonly left unclaimed after death?

Bank accounts, life insurance policies, forgotten 401k accounts, stocks and mutual funds, uncashed checks, and utility deposits. Life insurance and retirement accounts carry the highest balances and go unclaimed most frequently.

How does escheatment work and what happens to unclaimed assets after they transfer to the state?

After one to five years of inactivity, financial institutions are legally required to transfer dormant assets to the state. The state holds them as a custodian until a rightful heir files a claim, which most states allow indefinitely.

Can family members access a deceased person’s email account to find financial records after death?

Not easily. Google, Microsoft, and Yahoo each require a death certificate and proof of legal authority, and most will not provide login credentials even then. The process can take weeks or months with no guarantee of access.

What is the difference between a beneficiary designation and a will when it comes to unclaimed assets?

A beneficiary designation overrides the will entirely. Retirement accounts and life insurance policies transfer directly to whoever is named on the designation form, bypassing probate. An outdated designation from before a divorce or remarriage sends assets to the wrong person regardless of what the will says.

How do you create an asset inventory that actually stays current as your financial life changes?

A static document goes out of date the moment anything changes. A working inventory needs to capture new accounts automatically as they are opened. SmartHeritance’s SmartSync does this by scanning email correspondence from over 100 financial institutions periodically, without requiring any manual updates from the user.

References

National Association of Unclaimed Property Administrators (NAUPA). https://unclaimed.org/what-is-unclaimed-property/

Capitalize and Center for Retirement Research. “The True Cost of Forgotten 401(k) Accounts,” September 2025. https://www.hicapitalize.com/resources/the-true-cost-of-forgotten-401ks/

National Association of Insurance Commissioners (NAIC). “NAIC Life Insurance Policy Locator Tool Helps Consumers Connect with More Than $13 Billion in Benefits,” September 30, 2025. https://content.naic.org/article/naic-life-insurance-policy-locator-tool-helps-consumers-connect-more-13-billion-benefits

US Bureau of Labor Statistics. “Employee Tenure in 2024,” September 26, 2024. https://www.bls.gov/news.release/tenure.htm

Empathy. Cost of Dying research reports, 2022-2024. https://www.empathy.com/resourcesThe Hill. “States hold billions in unclaimed funds,” December 2025. https://thehill.com/homenews/nexstar_media_wire/5661389-states-hold-billions-in-unclaimed-funds-are-you-owed-any/