TL;DR

- Most families are not unprepared because they lack assets. They are unprepared because no one built a system that helps find those assets when something happens.

- A financial inventory is not a one-time document. It spans seven distinct Things, from retirement accounts and insurance policies to digital wallets and 2FA credentials, and it starts becoming outdated the moment you finish it.

- The standard advice to “write it down and put it somewhere safe” is a reasonable instinct with an incomplete design. Financial lives change constantly, and a static document cannot keep pace.

- Keeping the inventory current and getting it to your family at the right moment are two separate problems, and most approaches only partially address either one.

- This article walks through what a complete inventory actually covers, why static documents fail in practice, and what a system designed to stay current and reach your family actually looks like.

Introduction

Most people believe their family has a reasonable picture of where things stand financially. The data suggests otherwise.

In practice, financial complexity accumulates quietly over years, across dozens of institutions and platforms, and without a deliberate system to track it, the information that families need most becomes the hardest to find.

This is not a trust problem. It is a systems problem. Financial complexity accumulates quietly over years, across dozens of institutions and platforms, and without a deliberate system to track it, the information that families need most becomes the hardest to find.

The instinct to document everything is the right one. The problem is that treating documentation as a one-time task produces a record that is already drifting from reality by the time it is complete. This article covers what a complete financial inventory actually needs to include, why the standard approach breaks down in practice, and what a system designed around how financial lives actually work looks like.

Why Most Financial Inventories Fail Families

Every guide on family financial inventories arrives at roughly the same conclusion: make a list, organize it into categories, put it somewhere secure, and tell someone where it is. That advice is not wrong. It is incomplete in a way that turns out to matter quite a bit.

The problem is that this approach treats a dynamic situation as a static one. It produces a document calibrated to a person’s financial life on the day they created it, not the one they have two or three years later.

The Hidden Problem With Static Financial Records

The average person’s financial footprint today spans accounts across multiple banks, brokerages, insurance providers, retirement platforms, cloud services, digital wallets, and subscription services. Fifty years ago, a household’s finances might have fit on a single page. Today they are distributed across dozens of institutions and platforms, many of which generate no physical paper trail the family would naturally encounter.

Writing things down is the right instinct. The problem is that the document begins to drift from reality the moment it is finished. New accounts get opened. Passwords change. Beneficiary designations get updated after a marriage or the birth of a child, and sometimes not updated when they should be. A retirement account from a previous employer gets rolled over and gradually forgotten. Each of these changes creates a gap between what the inventory says and what is actually true.

When No One Knows Where Anything Is

The consequences of a missing or outdated inventory are well-documented. Most families who struggle after a loss are not ones where nothing was prepared. They are the ones where the person who managed everything carried it entirely in their head, and when they were gone, there was no map. Adult children describe spending months making calls to institutions, tracking down policy numbers, and piecing together accounts from old bank statements and email receipts. Retirement accounts sit inaccessible for years when beneficiary designations were never completed or updated. These situations are not rare. They are the predictable result of a financial life that was never documented in a form another person could actually use.

These are not unusual outcomes. They are what happens regularly when families are left to reconstruct a financial life they were never shown. Every one of them is preventable, but only if the solution is designed around how financial lives actually change over time.

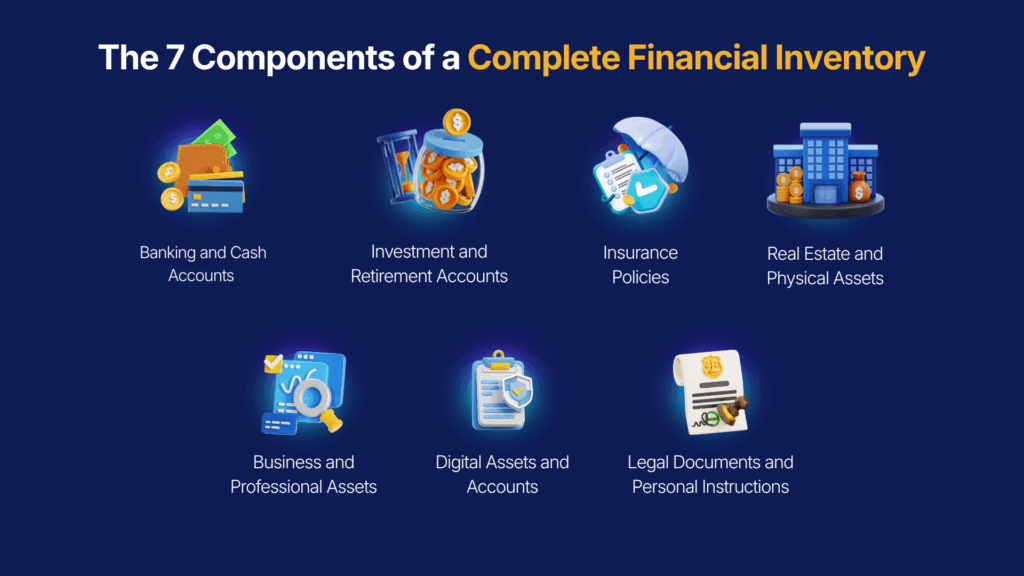

The 7 Components of a Complete Financial Inventory

To build a financial inventory that genuinely serves your family in a crisis, you need to plan for 7 components. Most inventories that exist in practice cover two or three.

Banking and Cash Accounts

This covers checking accounts, savings accounts, money market accounts, certificates of deposit, and safe deposit boxes. For each, the inventory should include the institution name, account number, and complete online access information, including where the safe deposit box key is physically stored.

The key distinction here is that this is not a list of balances. It is a complete access record structured so that another person could navigate it without you present.

Investment and Retirement Accounts

This covers brokerage accounts, 401(k) plans, IRAs, pension plans, employer equity and stock options, and Social Security enrollment records. For each, the inventory should include the institution, the account identifier, and the access credentials.

One element requires particular attention: beneficiary designations. These designations override the instructions in a will. A beneficiary named on a 401(k) from a previous employer will receive those funds regardless of what a will says, and families frequently discover too late that the designations on older accounts were never updated to reflect marriages, divorces, or deaths. A complete inventory documents not just where the accounts are, but what beneficiary designations currently exist on each one.

Insurance Policies

This covers life insurance (term and permanent), disability, long-term care, health, umbrella, homeowners, and auto policies. For each, the inventory should include the policy number, insurer name, agent contact information, and the account from which premiums are paid.

Life insurance is one of the most commonly lost financial assets. Policies purchased through agents who have since retired, documents stored in locations only the policyholder knew about, and policies taken out decades ago through employers or associations all represent real coverage that families fail to claim because they cannot locate the policy. A proactive record of what exists prevents this from happening.

Real Estate and Physical Assets

This covers properties owned, mortgage lenders and account information, vehicle titles, and significant physical valuables. The inventory should document where original deeds and titles are stored, including the location of any safe deposit box keys required to access them.

Business and Professional Assets

This covers business ownership interests, partnership agreements, intellectual property, and any asset that generates income or requires active management. It should also include contact information for the estate attorney, accountant, and financial advisor. These are the assets that create the most immediate operational complexity when the person managing them is no longer available.

Digital Assets and Accounts

This deserves more attention than most inventories give it, and it is where families encounter the most unexpected barriers. For a detailed breakdown of how digital assets work in the context of inheritance planning, the guide on digital estate planning covers this specifically.

The critical issue here is two-factor authentication. Most financial platforms, email providers, and cloud storage services now require 2FA as standard. If 2FA is tied to a deceased or incapacitated person’s locked mobile phone, the password becomes irrelevant. A complete digital inventory includes not only login credentials but 2FA backup codes for every account that uses them, and for each major platform, clear guidance on how to request access management in the event of death or incapacitation.

Legal Documents and Personal Instructions

This covers the will, trusts, power of attorney, healthcare directive, and advance directive. It should document the location of original copies and the name and contact information of the estate attorney.

It should also include something no legal document contains but families consistently say they needed: personal instructions. The context, preferences, and guidance that no will is written to provide — who should be called first, which decisions were most important, what the person wanted beyond the formal record of who receives what.

Challenge: Keeping Your Financial Inventory Current

If you have put the components together as mentioned above, you have an inventory your family can actually use. The next part is equally important: keeping it current as your finances change.

Why Your Financial Information Changes Faster Than Any Document Can Track

Consider how a typical financial life changes over two years. New accounts get opened. Passwords change. A refinance creates a new mortgage servicer. An insurance policy moves to a different provider. A subscription starts auto-debiting a card that has since been replaced. A retirement account from a former employer raises an unresolved rollover question.

Each of those changes creates a gap between what the inventory says and what is actually true. A static document created in good faith today may give a family incomplete or misleading information within months. Not because anyone failed to maintain it with care, but because maintaining a financial document requires remembering to update it every time something changes, and that is not a system anyone reliably sustains over years and decades.

What Happens When Financial Information Never Reaches Your Family

Accounts go unclaimed not because the assets were not real, but because the information never reached the people who needed it.

The accounts were real. The assets were legitimate. The information just never reached the people who needed it. For a full breakdown of how to prevent unclaimed assets and what recovery tools exist, the guide on preventing unclaimed assets after death goes into the specifics of state databases, NAUPA, and the National Registry of Unclaimed Retirement Benefits.

The point here is a maintenance point, not a recovery one. These assets exist in state treasuries because the financial map was never built or never kept current. The tools for finding them after the fact are reactive. The inventory is the proactive alternative.

The Difference Between a List and a System

| A List | A System | |

|---|---|---|

| Updates | Requires you to remember every time | Stays current automatically |

| Accounts | Only what you manually add | Captures new accounts as they appear |

| Over time | Drifts further from reality | Reflects where things actually stand |

| When something happens | Family has to find it | Reaches the right people automatically |

| Relies on | Your discipline | The platform doing the work |

From Inventory to System: What This Actually Requires

A complete financial inventory that functions as a genuine continuity plan has two requirements that go well beyond the seven-layer list: it has to stay current, and it has to reach your family when they need it. These are two separate design problems, and most approaches solve neither one fully.

The Discovery Problem: Why Financial Inventories Become Outdated

The most significant reason financial inventories fail is not that people lack the motivation to create them. It is that the maintenance burden is essentially invisible at the moment of creation and impossible to sustain manually over the years that follow.

Every financial account a person has ever opened has left a correspondence trail in email. Bank statements, policy confirmations, subscription receipts, investment notifications — all of it sits in inboxes across years of history that no one has thought to search systematically.

SmartHeritance addresses this maintenance problem through SmartSync, an AI-powered account discovery feature that connects to a user’s existing email and identifies correspondence from financial institutions, insurance providers, retirement platforms, subscription services, and digital wallets. Rather than relying on manual updates, the system scans for accounts that already exist in the email record, structures them into the continuity inventory, and continues scanning periodically so that new accounts are captured as they are opened. It is not a replacement for intentional organization. It is the mechanism that closes the gap between what a person’s financial life actually includes and what their inventory reflects.

The Delivery Problem: How Families Access Critical Information

A complete, current financial inventory that your family cannot access when they need it is not a continuity system. It is a well-organized document in a location no one can reach.

The question of who receives what information, at what level of detail, triggered by what event, and verified by whom is the question that every document-based approach leaves unanswered. It is also the question families find themselves unable to answer after a death or incapacity, because the person who set the system up is no longer available to activate it.

SmartHeritance’s Wellness Check Protocol addresses this delivery problem. It functions as the activation layer that most continuity planning ignores entirely – a proactive verification workflow that monitors for inactivity, confirms wellbeing, and releases the right information to designated recipients after a qualifying event has been verified. The family does not have to remember that the system exists or know where to log in. The system finds them, confirms what has happened, and delivers what they need.

Most families stop at the inventory. The ones who are genuinely prepared build the system around it.

Common Objections, Addressed Directly

“I Already Have a Will”

A will and a financial inventory solve different problems at different moments in the process. A will tells a court who should receive your assets. It does not tell your family where those assets are, how to access them, or what exists that they did not know about.

A will becomes operative after probate proceedings begin, a process that can take many months depending on the complexity of the estate and the jurisdiction. A financial inventory is what your family uses in the days, weeks, and months before and during that process to find what the will refers to. The distinction between legal documentation and operational continuity is covered in more depth in the guide on digital legacy planning versus estate planning.

“My Spouse Already Knows Everything”

The survey data on this is precise. Financial complexity accumulates over time, quietly and without announcement. Knowing that accounts exist and knowing how to locate, access, and claim them are different capabilities, and assuming the first means the second is already in place is the assumption that leaves families scrambling.

This is not a judgment on the quality of a relationship. It is a description of how financial complexity accumulates over time, quietly and without announcement. Knowing that accounts exist and knowing how to locate, access, and claim them are different capabilities, and assuming the first means the second is already in place is the assumption that leaves families scrambling.

“I Use a Password Manager”

A password manager addresses one part of one layer of the seven-layer inventory: access credentials for digital accounts. It does not cover account discovery for accounts no one knew existed, beneficiary designations, insurance policy locations, 2FA backup codes, or the coordination question of who receives what information and when. The specific limitations of password managers in a family continuity context are covered in detail in the guide on why password managers fall short for legacy planning.

“This Feels Overwhelming”

A complete financial inventory is a significant undertaking. But the overwhelm comes from approaching it as a one-time sprint, where the goal is to document everything in an afternoon. An inventory built as an incremental, living system, one that captures information as it is added and updates automatically where possible, is manageable in a way the sprint is not. The goal is to start the right way, not to finish everything in a single sitting.

“I Keep Meaning to Do This”

The families who say they wish they had done this sooner are not different from the families who kept meaning to. They are simply further along in the same story. The cost of not starting is invisible today. It becomes very visible later.

How to Get Started Without Getting Overwhelmed

Start With the Piece That Would Cause the Most Harm if Missing

Not all seven elements are equally urgent. For most families, the highest-stakes gaps are retirement account beneficiary designations, life insurance policy location and contact information, and at least one trusted person who knows where the core financial inventory is stored.

These are the areas where errors or omissions have the most irreversible consequences. Beneficiary designations that override a will. Insurance policies that expire unclaimed. Accounts that cannot be located because no one knew where to begin. Starting there, before building out the remaining components, addresses the most critical gaps first.

Treat It as a Living Document From Day One

From the day the inventory exists, build in a maintenance cadence. Quarterly or annual reviews are reasonable for most financial lives. The specific frequency matters less than the habit of treating major life events as triggers to update immediately: a new job, a home purchase, a marriage, a divorce, a new insurance policy, any significant account change. The inventory should be a practice, not a completed project.

Address the Access Question Before You Need To

The inventory is only as useful as its delivery system. Before the document is complete, the more important decisions are who has access to it, at what level of detail, and what event triggers that access. These decisions must be made while you are available to make them.

SmartHeritance was built around exactly this problem. Not just organizing financial information into a complete inventory, but ensuring the system stays current and reaches the right people at the right moment. If what you want is a system rather than a better list, the platform addresses both the maintenance problem and the delivery problem that most inventory approaches leave unresolved.

Helping Aging Parents Organize Their Financial Information

For aging parents, there is a window between the time they can still walk you through their financial life and the time they can no longer do that. This window is not always visible until it has already narrowed.

Having this conversation while it is still a collaboration is a fundamentally different experience than attempting to reconstruct a financial life afterward from institutional records, old statements, and guesswork. The first is a process. The second is an ordeal that routinely takes years.

The conversation does not have to begin with a formal financial review. It can begin with a single question: “If something happened to you and I needed to find your bank accounts, where would I start?” What comes after that becomes the foundation of the inventory.

SmartHeritance’s Parent Account feature allows an adult child to help a parent build and maintain their continuity record so the information is organized, private, and ready for the family before it is urgently needed rather than after. For broader context on why family continuity planning matters, particularly for families managing this across generations, the guide on family continuity planning covers this in full.

How SmartHeritance Solves the Two Problems Most Inventories Ignore

Every tool in this space addresses some version of the storage problem. SmartHeritance was built around the two problems that come after storage: keeping the inventory current without requiring constant manual effort, and getting it to the right people at the right moment without requiring your family to know where to look.

SmartSync handles the maintenance problem by turning the email correspondence trail that already exists into a structured, continuously updated financial record. Most people have years of account confirmations, policy documents, investment statements, and subscription receipts sitting in their inbox. SmartSync identifies what is there, organizes it into the inventory, and continues scanning so that new accounts are added as they appear. The record stays current because the system is doing the work, not the user.

The Wellness Check Protocol handles the delivery problem. It monitors for inactivity, reaches out proactively when something may be wrong, and releases the right information to designated family members only after a qualifying event has been verified. Your family does not have to remember that the system exists. They do not have to know where to log in or what to ask for. The platform finds them when the conditions you set are met.

The result is a family continuity system that functions the way a continuity plan should: quietly in the background while everything is fine, and exactly as intended when something changes. To understand how this fits into a broader personal legacy management approach, the guide on the Personal Legacy Manager covers the full platform context.

Visit smartheritance.com to build your family’s financial inventory as a system, not just a document.

Frequently Asked Questions

-

What is the difference between an estate planning inventory and a living trust?

An estate planning inventory records what you own and where it is. A living trust is a legal structure that distributes those assets. You need both.

-

How do I organize an estate planning inventory for multiple properties across different states?

Document each property separately with its deed, mortgage lender, and title details. Organize records by state since each state runs its own probate process.

-

Who should have access to my estate planning inventory while I am still alive?

Limit access to one or two trusted people who know where it is stored. Someone should always be able to locate it in an emergency.

-

What happens to an estate planning inventory when someone dies without a will?

The court appoints an administrator to manage the estate. A thorough inventory helps them locate and value everything without guesswork.

-

How do I document retirement accounts from a previous employer I no longer have records for?

Contact your former employer’s HR department or search the National Registry of Unclaimed Retirement Benefits at unclaimedretirementbenefits.com using your Social Security number.