TL;DR

- Most life insurance benefits go unclaimed not because coverage was missing, but because families could not find the policy, identify the insurer, or know what to file when the time came. Organize your documents now to close that gap before it becomes their problem.

- A single household often holds multiple separate policies: individual term or whole life, employer group coverage, supplemental elections, mortgage life, and association benefits. Each requires its own claim process, and your family needs specific details for each one to file successfully.

- Employer-provided group life insurance is the most commonly missed benefit because it lives entirely inside an HR portal and generates no paper the policyholder keeps. Document it separately and outside your employer’s systems.

- Beneficiary designations on life insurance policies override whatever a will says, so an outdated designation from a previous marriage or old job directly determines who receives the benefit, regardless of your current intentions.

- Reviewing your life insurance records once a year and after every major life event, including a job change, marriage, divorce, or new child, is what keeps the system from becoming outdated and useless when it matters most.

- SmartHeritance surfaces hidden policies, flags outdated beneficiary designations, and delivers your organized records to designated family members at the right moment, without them having to search for anything.

Introduction

Most people who buy life insurance do one thing right and one thing wrong. The right thing is that they purchase coverage. The wrong thing is that they assume the purchase itself is the plan.

The actual moment life insurance is meant to serve your family requires a completely different kind of preparation. Your beneficiaries need to know the policy exists, know which company holds it, have the policy number, know who to call, and have the documents required to file a claim. Without that information organized and accessible, the coverage you paid for may never reach them.

According to the NAIC, their Life Insurance Policy Locator has connected families with more than $10 billion in unclaimed life insurance and annuity benefits since launching in 2016. That figure represents coverage that was purchased and paid for, with specific beneficiaries named, that still required a government search tool to surface after the policyholder died.

This article covers exactly what to organize, why most current approaches miss critical policies, what your family needs to actually file a claim, and how to keep your records current so the system works when it matters.

Why Life Insurance Benefits Go Unclaimed

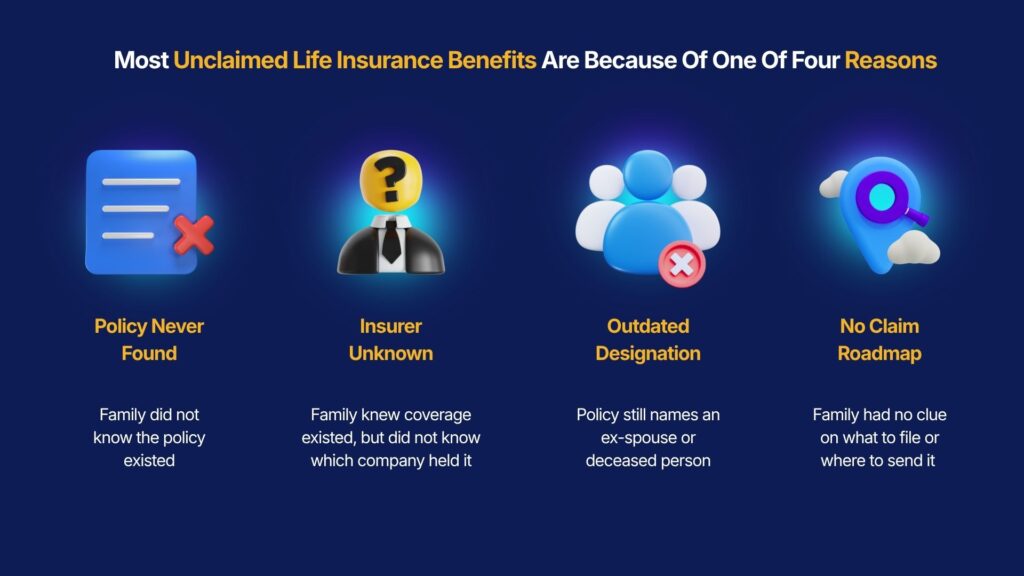

Before getting into the specifics of what to document, it helps to understand the actual failure points. When life insurance benefits go unclaimed, the reason almost always falls into one of four categories.

The family had no idea the policy existed: The LIMRA 2025 BEAT Study found that more than a third of U.S. workers, 36%, are not fully aware they have life insurance coverage through their employer. Employer-provided group life insurance is the most commonly missed benefit because it generates no paper the policyholder keeps and lives entirely inside an HR portal. If the policyholder never communicated this to their family, the family has no starting point for a claim.

The family knew coverage existed but had no way to identify the insurer: Knowing your parent had life insurance is very different from knowing they had a policy with a specific carrier, a policy number, and a dedicated claims line to call. The first piece of information acknowledges a benefit. The second piece enables a claim. Most families only have the first piece, which means they spend weeks searching manually, often without success.

The beneficiary designation was outdated: A policy purchased years ago may still name an ex-spouse, a deceased parent, or someone who predeceased the policyholder. Beneficiary designations on life insurance policies and retirement accounts override everything in a will. If the designation is wrong, the benefit does not automatically redirect to the intended person. According to an NAIC beneficiary preparedness survey, only 39% of Baby Boomers, 30% of Millennials, and 22% of Gen Z beneficiaries feel prepared for their role as a life insurance beneficiary, and a significant portion do not even know they have been named.

The beneficiary did not know what steps to take: Even when a family correctly identifies the insurer and the policy, the claims process requires specific documentation from that specific carrier. Without a record that spells out exactly what to submit and where to send it, families spend weeks assembling information that should have been documented in advance.

Organizing your life insurance records properly eliminates all four of these failure points before they become your family’s problem to solve.

What to Document for Every Policy You Hold

Most guides on this topic reduce the problem to “make a list.” The list is only as useful as what is on it. What your family needs is not just a reminder that a policy exists. They need enough specific information to file a claim successfully on the first attempt, with the right insurer, using the right process.

For every life insurance policy you hold, document the following in one accessible place.

- The insurer’s current name and the full policy number: Insurance companies are acquired, merged, and renamed regularly. The company name printed on a policy from 2010 may no longer be the operating entity. Include both the name on the original policy and the current operating name if the company has changed, so your family can locate the correct claims department without a detour.

- The dedicated claims contact, not the general service number: Most large carriers operate a separate claims department with its own phone number, mailing address, and online submission portal. The general customer service number will redirect your family, which adds time and friction during an already difficult period. Document the specific death claims contact at the time you are organizing, and verify it annually since these contacts change.

- The benefit amount, policy type, and active coverage dates: For term life policies, the expiration date determines whether the coverage is still in force. For employer group policies, document whether coverage continues after separation from the employer and under what conditions. A policy that lapsed before the policyholder died produces no benefit regardless of how well it was documented.

- The current beneficiary designations and when they were last updated: This is the piece most people assume is handled because they remember completing a form at enrollment years ago. What they do not track is whether the designation still reflects their current intent. Document who is named as primary and contingent beneficiary, along with the date it was last confirmed, so it is easy to identify when a review is overdue.

- Where the policy document lives and how to access it: Whether the policy is a physical document in a file cabinet, a PDF saved in an email account, or accessible only through an insurer’s online portal, document the specific location and the credentials needed to reach it.

- For employer group coverage, the HR contact and group carrier name: This detail requires its own entry because it is structurally different from individual policies. The employer acts as the intermediary in group life insurance claims. Your family needs to contact HR first, not the carrier directly, and HR can only help if there is documentation linking the coverage to the correct group policy. This information disappears when the employment relationship ends, which makes documenting it now, while still employed, the only reliable window to capture it. For a fuller breakdown of why employer coverage is the most overlooked benefit, read Legacy Planning as an Employee Benefit.

The Policies Most People Forget to Include

A life insurance inventory is only useful if it accounts for every policy in your household. Most people document the individual policy they consciously purchased and miss the ones that exist in the background of their financial life.

- Employer group life insurance typically provides one to two times annual salary in coverage, sometimes more with supplemental elections made at open enrollment. Because it exists entirely within the employer’s HR and benefits infrastructure, it generates no paper the policyholder keeps. A beneficiary looking for this policy has to contact the employer’s HR department, who will then connect them to the carrier. That process is slower and more complicated than it needs to be when nobody documented the carrier’s name in advance.

- Supplemental group life insurance is the additional coverage many employers offer beyond the base group policy, usually elected during open enrollment each year. It is a separate policy from the base group coverage, often underwritten by a different carrier, and is frequently overlooked entirely in post-death benefit searches because families did not know it existed as a separate line item.

- Mortgage life insurance is a decreasing term policy tied to the home loan, structured to pay off the remaining mortgage balance if the policyholder dies. This policy is held by the mortgage lender, not by the policyholder directly, so families searching for life insurance policies do not think to contact the lender. Many of these benefits go unclaimed for exactly this reason.

- Association and affiliation coverage includes accidental death and dismemberment policies, or small term life policies, offered through professional associations, credit unions, alumni organizations, and some credit card programs as member benefits. These are easy to forget because they are rarely the primary coverage and often require no medical underwriting or active management after enrollment.

- Converted or ported policies from previous employers are among the most commonly overlooked in a household inventory. When an employee leaves a job, group life insurance policies typically include a conversion option that allows the coverage to continue as an individual policy without a medical exam. People who exercised this option years ago may have an active policy they no longer actively track, with annual statements going to an email inbox that rarely gets checked.

What Your Family Needs to Actually File a Claim

Understanding the claims process shapes how you should organize your documents. Knowing a policy exists is not enough. Your family needs the specific information required to complete a claim with that particular insurer. Here is what most carriers require to process a death claim.

- Certified copies of the death certificate: Virtually every insurer requires certified copies, typically two to four, since each carrier needs its own. These must be certified copies from the vital records office in the state where the death occurred, not photocopies. Knowing in advance how many policies exist tells your family how many copies to order immediately after a death.

- A completed claimant statement on the insurer’s current form: Every carrier has its own form, and it must be the current version since outdated forms are rejected. Document where your family can find the current claim form for each insurer, whether that is an online portal or a number to call.

- The policy number: A beneficiary’s name alone is not a sufficient search parameter at most carriers. Without the policy number, the family has to prove the policy exists through other means, which adds significant delay to an already slow process.

- Proof of the beneficiary’s identity: A government-issued photo ID is required at submission by most carriers. It is a straightforward requirement, but one that needs to be on the list so it does not catch your family off guard.

- For employer group policies, the employer and carrier details: The claim process for group life insurance also requires the name of the employer, the name of the group insurance carrier, and the HR contact who handles benefits claims. The carrier cannot process a group life claim independently. The employer must confirm coverage first, which means your family needs to start with HR, not the insurer.

None of this information appears in a will, and none of it is automatically communicated alongside a death certificate. Every piece must be organized in advance, in a form your family can act on without having to search for it.

Why a Document Binder Falls Short

The standard recommendation is to put your important documents in a binder. It is a reasonable starting point and a meaningful improvement over nothing. It is also insufficient as a life insurance organization system, specifically because of how life insurance policies are structured today.

A binder works for documents you physically possess, but most life insurance coverage today does not produce documents the policyholder keeps. Employer group policies, supplemental elections, association benefits, and policies purchased through online portals all exist entirely in digital systems. A binder built around what you can print or file will systematically exclude these policies, which for many households represent a substantial portion of total coverage.

A binder also becomes outdated the moment your circumstances change. Policies lapse, employers change carriers, and beneficiary designations go unreviewed after a divorce. A binder reflects your situation on the day it was created and has no mechanism to update itself. A family relying on a binder from three years ago may be working from information that no longer accurately represents your coverage.

Finally, a binder is only useful to someone who knows it exists, knows where it is, and knows what to do with what they find. A document sitting in a home office filing cabinet is accessible to the person who put it there, but it may not reach an adult child who lives in another state, a spouse who was not involved in managing household finances, or an executor who has never been to the house.

For a detailed comparison between static document storage and a purpose-built life insurance organization system, read What Is a Personal Legacy Manager and Why You Need One.

When to Update Your Life Insurance Records

A life insurance document system that is accurate today can become misleading quickly. The following events each require an active review and update of your records.

- When you change jobs: Your group life insurance coverage changes entirely when you move to a new employer. The new employer has a different carrier, different benefit amounts, and a different enrollment process. The policy from your previous employer may have a portability or conversion option with a deadline you need to act on before it expires. Both situations require documentation at the time of the transition, not weeks later.

- After a marriage or divorce: Every beneficiary designation needs to be reviewed and explicitly updated after any change in marital status. A designation naming a current spouse remains in effect until it is changed, regardless of a subsequent divorce. Some states automatically revoke beneficiary designations after divorce, but this varies by state and policy type. Relying on state law rather than an explicit update is a risk that costs nothing to eliminate.

- When a child is born or adopted: Update the designation if you intend for that child to be a beneficiary or contingent beneficiary. Note that minor children cannot directly receive life insurance proceeds in most states. A custodian or trust must be named to hold the funds until the child reaches adulthood.

- When a named beneficiary dies: If a primary beneficiary predeceases the policyholder and no contingent beneficiary has been named, the proceeds may pay into the estate rather than directly to a person. This triggers probate and significantly delays the payout, which is avoidable with a simple designation update.

- When any policy changes: Whether you add coverage, let a policy lapse, convert a group policy, or purchase a new individual policy, update the documentation to reflect the current state of your coverage.

- Annually, regardless of other changes: Once per year, verify that every policy in your record is still active, that insurer contact information is current, and that beneficiary designations still reflect your intentions. This takes less time than most people expect and prevents the most common documentation failures. For a broader guide to what this process should cover, read How to Prevent Unclaimed Assets After Death.

How SmartHeritance Solves the Organization Problem

Organizing life insurance documents manually works if you do it completely, keep it current, store it somewhere accessible, and communicate its existence to the right people. Most households run into trouble on at least two of those four requirements, not from carelessness, but because the process has no built-in mechanism for staying current or for reaching the people who need it when the time comes.

SmartHeritance is built specifically to close each of those gaps for life insurance.

The SmartSync feature identifies every life insurance relationship in your digital records, including employer group policies, supplemental coverage, older policies that no longer generate active correspondence, and association benefits enrolled years ago and long forgotten. It builds a consolidated life insurance inventory that captures what a manual review would miss, because it looks at where policies actually leave digital traces rather than asking you to remember what you have.

Once your policies are surfaced and organized, SmartHeritance flags any beneficiary designations that appear outdated and provides the specific carrier contact and update process for each policy. This turns a vague annual reminder into a concrete action list with clear next steps for each entry.

The Wellness Check Protocol addresses the part that most organization systems ignore entirely, which is how the information actually reaches your family when it is needed. The protocol monitors for inactivity, confirms wellbeing, and proactively delivers your organized life insurance records to designated family members after verified confirmation of a death or incapacitation. Your family does not have to know the system exists or remember to look for it. The records come to them.

For context on how this approach fits within a broader family continuity framework, read Family Continuity Planning: What It Is and Why It Matters. If you are exploring this as a benefit for employees, see Financial Wellness Benefits for Employees.

Your family should receive what you put in place for them. Start organizing with SmartHeritance.

Frequently Asked Questions

-

Can an employer life insurance policy be claimed after leaving the job?

Only if you converted or ported the policy within the conversion window after leaving. Once that deadline passes, employer group coverage typically cannot be claimed.

-

How long does a life insurance company have to pay a death claim?

Most states require insurers to pay or deny a claim within 30 to 60 days of receiving all required documentation. Delays beyond that window typically accrue interest on the outstanding benefit.

-

Does a named beneficiary have to accept a life insurance payout?

No. A beneficiary can disclaim, meaning legally refuse, a life insurance payout, which then passes to the contingent beneficiary or into the estate depending on the policy terms.

-

What is the difference between a life insurance policy locator and a state unclaimed property database?

The NAIC Policy Locator contacts insurers on your behalf to find active policies before benefits are transferred to the state. State unclaimed property databases hold funds only after the insurer has already escheated them, meaning the claim process is slower and requires more proof.

-

Can a life insurance beneficiary be changed without the beneficiary knowing?

Yes. The policyholder can change a beneficiary designation at any time without notifying the current beneficiary. The person named has no legal right to be informed unless the policy has an irrevocable beneficiary designation.

References

- LIMRA 2025 BEAT Study: Facts About Life Insurance and Workplace Benefits

- NAIC: Life Insurance Tool Connects Consumers With More Than $10 Billion in Unclaimed Benefits, September 2024

- Michigan DIFS: Recovered More Than $8 Million in Life Insurance Benefits in 2024, May 2025

- NAIC Beneficiary Preparedness Survey, PR Newswire

- Trust & Will 2026 Estate Planning Report, Talker Research