TL;DR

- Most digital legacy guides cover wills, account inventories, and executor designations. That legal foundation matters, but it is not what your family needs to act during a crisis. The operational layer is what gets activated, and most families leave it entirely unbuilt.

- The five most commonly skipped steps are: planning for incapacity (not just death), building a release mechanism your family does not have to trigger manually, defining family coordination roles in advance, keeping records current without relying on discipline, and testing whether your plan actually works from your family’s perspective.

- According to the 2025 Caring.com Wills and Estate Planning Study, only 24% of Americans have a will in 2025, down from 33% in 2022. The problem is not just awareness. It is knowing what a complete, functional plan actually requires.

- After reading this guide, you will know exactly where your plan is complete and where to close the gap.

Introduction

Picture this scenario: a parent has a stroke and is alert but unable to communicate clearly. An adult child is standing in a hospital corridor trying to figure out which insurance policy covers the ICU stay, which accounts are on autopay and might lapse, and whether they have any legal authority to act on their parent’s behalf. There is a will filed somewhere with an attorney, a password manager on the parent’s phone, and no one in the family who knows either the attorney’s contact or the master password. Nobody knows where to start.

This is not a hypothetical. It plays out in families across the country every year, often in families that believed they had already done the preparation work.

Most digital legacy planning guides cover the legal layer well: wills, account inventories, digital executor designations, and platform-specific legacy contacts. That foundation matters. But beneath the legal layer sits an operational layer that determines whether your family can actually act when something happens. Account discoverability, incapacity planning, family coordination, information release, and ongoing maintenance are what get activated during a crisis, and they are almost entirely absent from most guides and most family plans.

This guide covers both layers across ten steps. Steps 1 through 5 address the legal and organizational foundation. Steps 6 through 10 address the operational layer where virtually every existing guide stops too early. If you want to understand how digital legacy planning differs from estate planning more broadly, our Digital Legacy Planning vs. Estate Planning explainer covers that distinction in detail.

Why Most Digital Legacy Plans Fail When Families Actually Need Them

Current guides in this space cover what matters legally: understanding what digital assets are, building a document inventory, designating an executor, assigning legacy contacts on platforms like Google and Apple, and understanding the legal framework around digital access after death. These are necessary components of a complete plan.

The problem is where they stop.

According to the 2025 Caring.com Wills and Estate Planning Study, which surveyed over 2,500 American adults, only 24% of Americans have a will today, down from 33% in 2022. The Trust and Will 2025 Estate Planning Report, drawing from 10,000 respondents, found that 55% of Americans have no estate documents at all. The gap is not primarily a knowledge problem. Most people who have done something believe they are operationally prepared when they are not.

Here is the distinction that matters:

Legal planning answers one question: who receives what?

Operational planning answers a completely different set of questions:

- What does my family actually do on day one of a crisis?

- Which accounts exist that they do not know about?

- Who handles what if I am incapacitated but not deceased?

- How does the information reach them if they do not know where to look?

Most guides only build an answer to the first question while leaving the rest entirely unaddressed. This guide covers both layers, with specific attention to the five operational steps that most families leave entirely unbuilt.

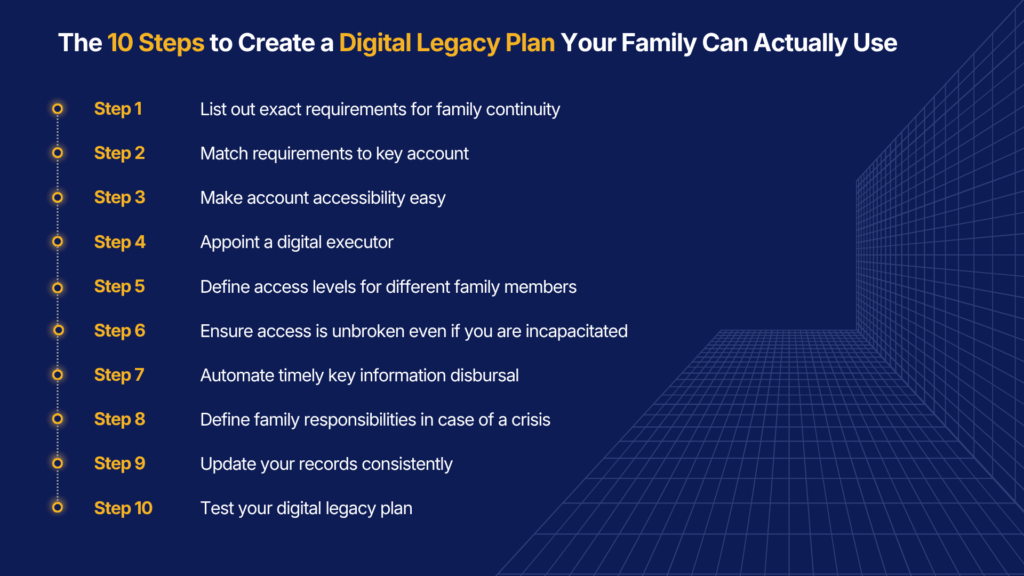

The 10 Steps to Create a Digital Legacy Plan Your Family Can Actually Use

The first five steps cover ground that thoughtful preparedness demands, and some readers will have completed parts of them already. Steps 6 through 10 address the layer where most plans stop too early. The second half is where the real gaps tend to live.

Step 1: Know What Your Family Will Need

Before building anything, it is worth being precise about scope because most people underestimate how many categories a complete digital legacy plan needs to address:

- Financial and Legal: Bank accounts, investment and retirement accounts, insurance policies across all types, property records, wills, trusts, powers of attorney, tax documents, and any outstanding loans or liabilities.

- Digital Accounts and Subscriptions: Email accounts, cloud storage, social media, streaming services, recurring subscriptions, digital wallets, and cryptocurrency. This category grows faster than most people actively track.

- Healthcare and Identity: Advance healthcare directives, medical records access information, health insurance details, Medicare or supplemental coverage documentation, and government identification records.

- Business and Professional: Business ownership documents, professional licenses, employment benefits, equity agreements, and any contractor relationships with ongoing financial implications.

- Personal and Sentimental: Digital photo libraries, personal correspondence, creative files, recorded messages, and any instructions or wishes your family should have access to.

One diagnostic question cuts across all five categories: in each of these areas, could your family locate what they need in under ten minutes, without your help? If the answer is uncertain in even one category, the plan has a specific gap that needs to be closed.

According to the National Association of Unclaimed Property Administrators (NAUPA), roughly 1 in 7 Americans have unclaimed property sitting in state programs, and the primary reason assets go unclaimed is not legal complexity but that families simply could not find what already existed. Scope clarity is the first line of defense against that outcome.

For a detailed checklist of what to include in each category, see our estate planning inventory guide.

Step 2: Find Every Account That Matters

This is where most plans break down before they are even fully built, and for a structural reason that has nothing to do with personal discipline.

Research consistently suggests the average person maintains well over 100 digital accounts across banks, investment platforms, insurance providers, subscriptions, cloud services, and digital wallets. These accounts accumulate over years:

- Employer retirement platforms from previous jobs that nobody transferred

- Investment accounts opened briefly and rarely revisited

- Insurance policies purchased through agents who have since moved on

- Subscriptions tied to payment methods that nobody actively monitors anymore

The problem with building an inventory manually is straightforward. You can only write down what you remember, and what you do not remember, your family cannot find.

There is a more reliable starting point. Every financial account, insurance policy, subscription service, and investment platform generates email correspondence, which means that inbox contains a more complete map of your financial life than any spreadsheet you have maintained, because it captures accounts you have stopped actively thinking about alongside the ones you manage regularly.

How SmartSync solves this:

SmartHeritance’s SmartSync connects to your existing email account and scans for correspondence from financial institutions, insurance providers, retirement platforms, investment services, cloud storage providers, digital wallets, and subscription services. It identifies accounts that have left a trail in your inbox, organizes them into structured records, and presents them for your review before anything is stored. Personal emails are never accessed or retained.

When SmartSync runs against a real inbox, users consistently surface accounts they had genuinely stopped tracking, including retirement accounts from previous employers, insurance policies purchased years ago, and subscription services still auto-billing on a card nobody actively manages. After the initial scan, SmartSync continues running periodically, identifying new accounts as they are opened and adding them to the record without requiring any manual input.

Two common objections come up at this step:

“My spouse already knows everything”: In practice, they know what they have been told about and do not have visibility into accounts that accumulated over years without active communication. This is not a gap in the relationship but simply how financial life grows.

“I use a password manager”: Password managers only store credentials for accounts you have manually added and cannot discover accounts you never entered. If your family does not know the master password, the password manager becomes the first barrier rather than the first solution. Our dedicated piece on password manager limitations covers this gap in full.

The broader consequence of discoverability failure shows up at population scale. According to NAUPA’s Fiscal Year 2024 Annual Report, unclaimed property programs returned $4.49 billion to rightful owners in a single year, representing only a fraction of what remains unclaimed. At the household level, this translates to weeks or months of institutional calls and document requests during grief or a medical emergency. Our guide on preventing unclaimed assets covers how this plays out in practice.

Step 3: Make Important Documents Easy to Access

The document categories that matter in a crisis are well established:

- Will and any codicils

- Healthcare directive and living will

- Durable power of attorney

- Insurance policies across all types

- Investment and retirement account summaries

- Property records and deeds

- Tax records for recent years

- Business documents where applicable

The organizing question most people skip is whether their family can actually reach these documents when they need them. A will stored in an attorney’s office that your family does not know about is not a functional document during a medical emergency, and a healthcare directive filed in a physical location that no one has been shown is equally inaccessible when the moment arrives. The documents exist, but the access does not.

The standard to aim for: if you were unreachable tomorrow, could your family locate any of these documents within ten minutes, without your assistance?

The answer should not depend on anyone’s ability to remember where things are. It should depend on a designated location, physical or digital, that the right family members know about and can navigate independently.

This matters financially in ways that are often underestimated. Healthcare directives and powers of attorney that cannot be located create immediate operational consequences including delayed medical decisions, the possibility of court intervention to establish legal authority, and costs that accrue when the legal mechanism exists but cannot be found when needed.

Step 4: Choose Who Will Manage Your Digital Estate

A digital executor is the person responsible for managing your digital estate after your death or incapacity. In practice, their responsibilities include:

- Closing or memorializing accounts according to your wishes

- Managing digital assets with financial value through estate settlement

- Handling content with sentimental significance

- Interacting with platforms and institutions on behalf of the estate

Some families designate the same person as both their traditional executor and their digital executor, while others separate the roles based on capability, proximity, or relationship. What matters is that someone is designated and clearly understands what they are specifically responsible for.

The legal framework supporting this designation has expanded substantially. As of 2024, 46 states and Washington D.C. have enacted the Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA), which provides a legal basis for digital executor authority. Understanding how this applies in your state is a matter for an estate attorney.

The key operational point here: the legal designation itself is not a plan. A named digital executor who does not know what accounts exist, where credentials are held, or what order to address things still starts from zero on day one. The designation is necessary, but the operational system that makes it functional is what most plans leave unbuilt.

Step 5: Decide Who Gets Access to What

Not everyone in your family needs access to everything, and treating access as a simple binary where either someone has it or they do not creates both gaps and conflicts.

A category-based access model works significantly better:

| Recipient | What They Need Access To |

| Spouse | Financial accounts, outstanding obligations, recurring bills |

| Healthcare proxy | Medical directives, health insurance, care instructions |

| Adult child | Specific documents, personal materials, property records |

| Sibling or close family | Sentimental records, personal correspondence |

| Digital executor | Account credentials, platform access, digital assets |

These categories are legally and practically distinct from each other. Financial access for an executor operates under different conditions than healthcare access for a proxy, which in turn is different from personal access for a family member.

The coordination risk of not structuring this explicitly is twofold: either no one has access when they need it, or multiple people try to act simultaneously without defined roles, creating delays and in some family dynamics genuine conflict.

SmartHeritance allows users to designate trusted recipients by category, specifying what each person can see and under what conditions. Information is not released until the conditions the user established are verified, which resolves the access governance question that most plans leave entirely implicit. Implicit access arrangements work adequately in uncomplicated family dynamics, but in the dynamics that actually exist across blended families, estranged siblings, and geographically dispersed adult children, they frequently do not.

Step 6: Plan for Incapacity Specifically, Because Most Plans Ignore It Entirely

The planning failure most families discover is not death without a will. It is incapacity without a system.

Consider what a family faces when a parent has a stroke and is alive but unable to communicate clearly. Bills need to be paid, insurance policies need to be maintained, investment accounts need managing, healthcare decisions need to be made, and ongoing care needs to be coordinated. The family may have no legal authority to act and no knowledge of where anything is, because the systems and accounts that run a household do not pause for a medical crisis.

Why most existing plans fail here:

- A will provides no guidance during incapacity

- A password manager requires knowing the master password to be useful

- The typical estate plan assumes a clean transition from full capacity to death

- Most legal documents are activated by death, not by incapacity

A complete incapacity plan requires four specific elements:

- A current, accessible durable power of attorney that relevant family members know about and can produce on short notice

- Healthcare directives that can be located and presented to medical providers quickly

- An operational system that can be activated without the primary person’s involvement

- Family members who understand their role before a crisis, not during it

The financial consequences of an unplanned incapacity event are measurable. Bills go unpaid, automatic payments fail, insurance policies lapse because no one knew they required active management, and accounts may be frozen pending legal intervention. Court-ordered guardianship, when a family has no legal authority to act, carries significant cost and delay that an organized, activated plan eliminates entirely.

Step 7: Make Information Reach Your Family Automatically

Most legacy planning systems are passive. Information is stored somewhere and when a crisis occurs, the family must discover that the information exists, locate it, and access it while simultaneously managing a medical emergency or processing grief. That design assumption fails in the scenarios that matter most.

The design principle most legacy systems miss:

The goal is not storing information your family can find. The goal is a system that delivers information to the right people when conditions are verified, without requiring the family to trigger the process from scratch.

How the SmartHeritance Wellness Check Protocol works:

- User remains active on SmartHeritance: system monitors normally, no action taken

- Sustained inactivity detected: system sends a proactive check-in to the user

- User does not respond: system contacts designated family members

- Family confirms a significant event and provides verification

- System releases designated information to designated recipients, according to conditions set in advance

The family does not need to discover that a platform exists, and they do not need to navigate a login they have never used before. Without a release mechanism like this, a family that wants to access an incapacitated parent’s organized continuity records still has to find them, access them, and know what to do with them during exactly the period when none of those tasks should be their burden.

Step 8: Assign Family Roles Before a Crisis Happens

Most families default to whoever steps forward first or whoever happens to be physically present when a crisis occurs, and without a defined coordination plan that approach creates duplication, missed steps, and in some cases conflict during the moment when none of those outcomes are acceptable.

What a coordination plan needs to define:

- Who is the primary contact for financial matters

- Who is the primary contact for healthcare decisions

- What category of tasks gets addressed in what order during the first week

- Who has access to what information and under what conditions

- Who communicates with which institutions and advisors

When family members are figuring out their roles in real time during a crisis, some will duplicate effort, others will wait to understand what they are supposed to do, and critical tasks in unfamiliar categories can go missed entirely. A documented coordination plan eliminates all of this because roles were defined before the crisis, not during it.

The sibling dynamic is worth naming specifically. The absence of a defined coordination structure is one of the most common sources of family tension during estate settlement, and the tension is rarely directly about money. It is about authority, information access, and role ambiguity during a high-stress period. A documented coordination plan removes that ambiguity before it has a chance to become conflict.

For adult children helping an aging parent organize their plan, SmartHeritance’s Parent Account model allows an adult child to have coordinated visibility into a parent’s continuity plan without full access to sensitive credentials, enabling preparation without the complications that come from unstructured full access.

Step 9: Keep Your Plan Updated as Life Changes

A plan built today reflects today’s financial life, and without a maintenance system it becomes progressively less accurate over time in a way that is entirely invisible until a family is already trying to find things during a crisis.

Why financial records drift out of date:

- New investment accounts get opened without updating any record

- Insurance providers change during annual renewals

- Subscriptions accumulate on payment methods nobody monitors

- Financial advisors rotate without new contact details being documented

- Beneficiary designations are never updated after major life events

Manual maintenance requires consistent discipline across years and decades, and almost no one sustains this without a structural prompt. This is not a personal failure but a design flaw in most legacy planning systems, which assume that once built, a plan remains accurate indefinitely without any active maintenance mechanism.

How SmartSync handles ongoing maintenance:

Because SmartSync remains connected to a user’s email after the initial setup, it continues scanning periodically, automatically identifying new accounts as they appear and adding them to the legacy record without requiring any manual input. When a new financial account is opened and a confirmation email arrives, SmartSync captures it. The record updates because financial life updates, not because the user remembered to go back and add something manually.

For elements that do not come through email, such as property records or physical assets, SmartHeritance runs periodic reminders that prompt users to review and add those details over time.

What to review manually, and when:

- Beneficiary designations: once a year

- All documents: after any major life event including marriage, divorce, a new employer, new property, or a change in financial advisor

Outdated beneficiary designations are among the most common and costly estate planning failures because they pass assets to outdated designees regardless of what a will or trust instructs. Combining an automated maintenance system with a structured annual review eliminates most of that risk.

Step 10: Test Whether Your Plan Actually Works

The final step is a perspective shift. The question is not whether the information exists in your plan but whether your family can find it, access it, and know what to do with it without you available to help.

Three questions that test whether your plan actually works:

- Question 1: If you were unreachable tomorrow, who would your family contact first, and would that person know exactly what to do?

- Question 2: Could your family identify all of your financial accounts within one week, including accounts you rarely think about?

- Question 3: Is there a scenario, whether incapacity, temporary cognitive impairment, or a sudden medical emergency, for which your current plan has no defined answer?

Most plans fail at least one of these questions, and that is the purpose of the test. A plan that fails one question needs a specific targeted addition rather than a complete rebuild, and identifying the gap clearly is what makes it possible to close it efficiently.

A plan that passes all three meaningfully reduces professional fees during estate settlement, prevents asset discovery failure, and eliminates the cost of court intervention when authority and access are unclear from the outset.

A List and a System Are Not the Same Thing

This distinction explains why most well-intentioned plans still leave families unprepared when it actually matters.

| A List | A System |

| Records what exists today | Updates as financial life changes |

| Goes out of date silently | Maintained through automated scanning |

| Passive: family has to find it | Active: delivers information when conditions are met |

| Does not coordinate people | Structures access by recipient and category |

| Fails in unplanned scenarios | Designed for scenarios the builder did not anticipate |

Most legacy plans are lists. They are built once, stored somewhere, and expected to remain useful indefinitely, but they do not update themselves, they do not reach anyone when needed, they do not coordinate multiple family members under stress, and they do not address scenarios the builder did not specifically anticipate.

A system requires four things that a list does not provide:

- A mechanism for staying current as financial life changes (SmartSync handles this)

- A mechanism for reaching the right people at the right time (Wellness Check Protocol handles this)

- A structure for coordinating family members with different roles (recipient permissions handle this)

- A design that works in scenarios the builder did not plan for

SmartHeritance is a Family Continuity Planning platform built around this distinction. It functions as the operational layer between having an estate plan and your family being able to act on it. It is not a document vault, a password manager, or a will replacement. To understand how this positions differently from what traditional estate planning provides, see our family continuity planning overview and our personal legacy manager explainer.

The operational gap between a list and a system is measurable in estate settlement time, professional fees, unclaimed assets, and the administrative burden families carry during the most difficult periods they face together.

How SmartHeritance Helps Families Stay Prepared

SmartHeritance is built specifically around the steps that most estate plans and most digital legacy guides leave incomplete.

What each core feature addresses:

- SmartSync solves the account discoverability problem by scanning the email trail your financial life has already generated, surfacing accounts your family would need to locate without any manual inventory effort on your part

- Wellness Check Protocol solves the release mechanism problem, ensuring that organized information reaches your designated family members without them needing to search for it

- Permission-based recipient model solves the coordination problem by giving each family member access to the specific categories they need under the conditions you set

- Parent Account enables adult children to help aging parents organize their continuity record without requiring the parent to manage the platform independently

If you want to see where your own plan has gaps, start with account discoverability. Connect your email to SmartHeritance and run SmartSync. It takes a few minutes and surfaces what no manual spreadsheet can: the accounts that exist in your financial life but not yet in your family’s awareness.

Most families discover the gap in their plan at the worst possible moment. Visit www.smartheritance.com to close it before that moment arrives.

References

- 2025 Caring.com Wills and Estate Planning Study: www.caring.com/resources/wills-survey

- 2025 Trust and Will Estate Planning Report (PRNewswire, February 25, 2025): www.prnewswire.com/news-releases/comprehensive-2025-trust–will-estate-planning-report-reveals-the-american-dream-in-crisis-302384026.html

- NAUPA Fiscal Year 2024 Annual Report: nast.org/wp-content/uploads/naupa-release-annual-report-oct-29-2024.pdf

- RUFADAA State Adoption Data, IronClad Family 2026: ironcladfamily.com/blog/digital-legacy-planning-checklist-protecting-your-digital-dna-in-2026